Facebook has finally revealed the details of its cryptocurrency Libra, which will let you buy things or send money to people with nearly zero fees. You’ll pseudonymously buy or cash out your Libra online or at local exchange points like grocery stores, and spend it using interoperable third-party wallet apps or Facebook’s own Calibra wallet that will be built into WhatsApp, Messenger, and its own app. Today Facebook released its white paper explaining Libra and its testnet for working out the kinks of its blockchain system before a public launch in the first half of 2020.

Facebook won’t fully control Libra, but instead get just a single vote in its governance like other founding members of the Libra Association including Visa, Uber, and Andreessen Horowitz who’ve invested at least $10 million each into the project’s operations. The association will promote the open-sourced Libra blockchain and developer platform with its own Move programming language plus sign up businesses to accept Libra for payment and even give customers discounts or rewards. Facebook is launching a subsidiary company also called Calibra that handles its crypto dealings and protects users’ privacy by never mingling your Libra payments with your Facebook data so it can’t be used for ad targeting. Your real identity won’t be tied to your publicly visible transactions. But Facebook/Calibra and other founding members of the Libra Association will earn interest on the money users cash in that is held in reserve to keep the value of Libra stable.

Facebook’s audacious bid to create a global digital currency that promotes financial inclusion for the unbanked actually has more privacy and decentralization built in than many expected. Instead of trying to dominate Libra’s future or squeeze tons of cash out of it immediately, Facebook is instead playing the long-game by pulling payments into its online domain. Facebook’s VP of blockchain David Marcus explains the company’s motive and the tie-in with its core revenue source, telling me “if more commerce happens, then more small business will sell more on and off platform, and they’lll want to buy more ads on the platform so it will be good for our ads business.”

The Risk And Reward Of Building The New PayPal

In cryptocurrencies, Facebook saw both a threat and an opportunity. They held the promise of disrupting how things are bought and sold by eliminating transaction fees common with credit cards. That comes dangerously close to Facebook’s ad business that influences what is bought and sold. If a competitor like Google or an upstart built a popular coin and could monitor the transactions, they’d learn what people buy and could muscle in on the billions spent on Facebook marketing. Meanwhile, the 1.7 billion people who lack a bank account might choose whoever offers them a financial services alternative as their online identity provider too. That’s another thing Facebook wants to be.

Yet existing cryptocurrencies like Bitcoin and Ethereum weren’t properly engineered to scale to be a medium of exchange. Their unanchored price was susceptible to huge and unpredictable swings, making it tough for merchants to accept as payment. And cryptocurrencies miss out on much of their potential beyond speculation unless there are enough places that will take them instead of dollars, and the experience of buying and spending them is easy enough for a mainstream audience. But with Facebook’s relationship with 7 million advertisers and 90 million small businesses plus its user experience prowess, it was well poised to tackle this juggernaut of a problem.

Now Facebook wants to make Libra the evolution of PayPal. It’s hoping Libra will become simpler to set up, more ubiquitous as a payment method, more efficient with fewer fees, more accessible to the unbanked, more flexible thanks to developers, and more long-lasting through decentralization.

“Success will mean that a person working abroad has a fast and simple way to send money to family back home, and a college student can pay their rent as easily as they can buy a coffee” Facebook writes in its Libra documentation. That would be a big improvement on today, when you’re stuck paying rent in insecure checks while exploitative remittance services like charge an average of 7% to send money abroad, taking $50 billion from users annually. Libra could also power tiny microtransactions worth just a few cents that are infeasible with credit card fees attached, or replace your pre-paid transit pass.

If Facebook succeeds and legions of people cash in money for Libra, it and the other founding members of the Libra Association could earn big dividends on the interest. And if suddenly it becomes super quick to buy things through Facebook using Libra, businesses will boost their ad spend there. But if Libra gets hacked or proves unreliable, it could cost lots of people around the world money while souring them on cryptocurrencies. And by offering an open Libra platform, shady developers could build apps that snatch not just people’s personal info like Cambridge Analytica, but their hard-earned digital cash.

How Does Libra Work?

By now you know the basics of Libra. Cash in a local currency, get Libra, spend them like dollars without big transaction fees or your real name attached, cash them out whenver you want. Feel free to stop reading and share this article if that’s all you care about. But the underlying technology, the association that governs it, the wallets you’ll use, and the way payments work all have a huge amount of fascinating detail to them. Facebook has released over 100 pages of documentation on Libra and Calibra, and we’ve pulled out the most important facts. Let’s dive in.

The Libra Association – Crypto’s New Oligarchy

Facebook knew people wouldn’t trust it to wholly control the cryptocurrency they use, and it also wanted help to spur adoption. So Facebook recruited the founding members of the Libra Association, which oversees the development of the token, the reserve of real-world assets that gives it value, and the governance rules of the blockchain. Each founding member paid a minimum of $10 million to join and optionally become a validatory node operator (more on that later), gain one vote in the Libra Association council, and be entitled to a share (proportionate to their investment) of the dividends from interest earned on the Libra reserve users pay fiat currency into to receive Libra.

The 28 soon-to-be founding members of the association and their industries, previously reported by The Block’s Frank Chaparro, include:

- Payments: Mastercard, PayPal, PayU (Naspers’ fintech arm), Stripe, Visa

- Technology and marketplaces: Booking Holdings, eBay, Facebook/Calibra, Farfetch, Lyft, Mercado Pago, Spotify AB, Uber Technologies, Inc.

- Telecommunications: Iliad, Vodafone Group

- Blockchain: Anchorage, Bison Trails, Coinbase, Inc., Xapo Holdings Limited

- Venture Capital: Andreessen Horowitz, Breakthrough Initiatives, Ribbit Capital, Thrive Capital, Union Square Ventures

- Nonprofit and multilateral organizations, and academic institutions: Creative Destruction Lab, Kiva, Mercy Corps, Women’s World Banking

Facebook says it hopes to reach 100 founding members before the official Libra launch and it’s open to anyone that meets the requirements including direct competitors to like Google or Twitter.

To join, members must have a half rack of server space, a 100mbps or above dedicated internet connection, a full-time site reliability engineer, and enterprise-grade security. Businesses must hit two of three thresholds of a $1 billion USD market value or $500 million in customer balances, reach 20 million people a year, and/or be recognized as a top 100 industry leader by a group like Interbrand Global or the S&P.

Crypto-focused investors must have over $1 billion in assets under management, while Blockchain businesses must have been in business for a year, have enterprise grade security and privacy, and custody or staking greater than $100 million in assets. And only up to one-third of founding members can by crypto-related businesses or invidually invited exceptions. Facebook also accepts research organizations like universities, and non-profits fulfilling three of four qualties including working on financial inclusion for over five years, multi-national reach to lots of users, a top 100 designation by Charity Navigator or something like it, and/or $50 million in budget.

The Libra Association will be responsible for picking recruiting more founding members to act as validator nodes for the blockchain, fundraising to jumpstart the ecosystem, designing incentive programs to reward early adopters, and doling out social impact grants. A council with a representative from each member will help choose the association’s managing director who will appoint an executive team, elect a board of 5 to 19 top representatives.

Each member including Facebook/Calibra will only get up to one vote or 1% of the total vote (whichever is larger) in the Libra Association council. This provides a level of decentralization that protects against Facebook or any other player hijacking Libra for its own gain.

The Libra Currency – A Stablecoin

A Libra is a unit of the Libra cryptocurrency that’s represented by a three wavy horizontal line unicode character like the dollar is represented by $. The value of a Libra is meant to stay largely stable so it’s a good medium of exchange since merchants can be confident they won’t be paid a Libra today that’s then worth less tomorrow. The Libra’s value is tied to a basket of bank deposits and short-term government securities for a slew of historically stable international currencies including the dollar, pound, europ, swiss franc, and yen. The Libra Association maintains this basket of assets and can change the balance of its composition if necessary to offset major price fluctuations in any one foreign currency so that the value of a Libra stays consistent.

The Libra Association is still hammering out the exact start value for the Libra, but it’s meant to somewhere close to the value of a dollar, euro, or pound so it’s easy to conceptualize. That way, a gallon of milk in the US might cost 3 to 4 Libra, similar but not exactly the same as with dollars.

The idea is that you’ll cash in some money and keep a balance of Libra that you can spend at accepting merchants and online services. You’ll be able to trade in your local currency for Libra and vice versa through certain wallet apps including Facebook’s Calibra, third-party wallet apps, and local resellers like convenience or grocery stores where people already go to top-up their mobile data plan.

The Libra Reserve – One For One

Each time someone cashes in a dollar or their respective local currency, that money goes into the Libra Reserve and an equivalent value of Libra is minted and doled out to that person. If someone cashes out from the Libra Association, the Libra they give back are destroyed/burned and they receive the equivalent value in their local currency back. That means there’s always 100% of the value of the Libra in circulation collateralized with real world assets in the Libra Reserve. It never runs fractional. And unliked “pegged” stable coins that are tied to a single currency like the USD, Libra maintains its own value — though that should cash out to roughly the same amount of a given currency over time.

When Libra Association members join and pay their $10 million minimum, they receive Libra Investment Tokens. Their share of the total tokens translates into the proportion of the dividend they earn off of interest on assets in the reserve. Those dividends are only paid out after Libra Association uses interest to pay for operating expenses, investments in the ecosystem, engineering research, and grants to non-profits and other organizations. This interest is part of what attracted the Libra Association’s members. If Libra becomes popular and many people carry a large balance of the currency, the reserve will grow huge and earn significant interest.

The Libra Blockchain – Built For Speed

Every Libra payment is permanently written into the Libra blockchain — a cryptographically authenticated database that acts as a public online ledger designed to handle 1000 transactions per second. The blockchain is operated and constantly verified by founding members of the Libra Association who each invested $10 million or more for a say in the cryptocurrency’s governance and the ability operate a validator node.

When a transaction is submitted, each of the nodes runs a calculation based on the existing ledger of all transactions. Thanks to a Byzantine Fault Tolerance system, just two-thirds of the nodes must come to consensus that the transaction is legitimate for it to be executed and written to the blockchain. A structure of Merkle Trees in the code makes it simple to recognize changes made to the Libra blockchain.

Transactions on Libra cannot be reversed. If an attack compromises over one-third of the validator nodes causing a fork in the blockchain, the Libra Association says it will temporarily halt transactions, figure out the extent of the damaage, and recommend software updates to resolve the fork.

Transactions aren’t entirely free. They incur a tiny fraction of a cent fee to pay for “gas” that covers the cost of processing the transfer of funds similar to with Ethereum. This fee will be negligible to most consumers, but when they add up the gas charges will deter bad actors from creating millions of transactions to power spam and denial-of-service attacks.

Move Coding Language – For Moving Libra

The Libra blockchain is open source with an Apache 2.0 license and any developer can build apps that work with it using the Move coding language. The blockchain’s prototype launches its testnet today, so it’s effectively in developer beta mode until it officially launches in the first half of 2020. The Libra Association is working with HackerOne to launch a bug bounty system later this year that will pay security researchers for safely identifying flaws and glitches. In the meantime, the Libra Association is implementing the Libra Core using the Rust programming language since it’s designed to prevent security vulnerabilities, and the Move language isn’t fully ready yet.

Move was created to make it easier to write blockchain code that follows an author’s intent without introducing bugs. It’s called Move because its primary function is to move Libra coins from one account to another, and never let those assets be accidentally duplicated. The core transaction code looks like “LibraAccount.pay_from_sender(recipient_address, amount) procedure”. Eventually, Move will be able to create smart contracts for programmatic interactions with the Libra blockchain. Until Move is ready, developers can create modules and transaction scripts for Libra using Move IR, which is high-level enough to be human-readable but low-level enough to be translatable into real Move bytecode that’s written to the blockchain.

The Libra ecosystem and the Move language will be completely open to use and build, which presents a sizable risk. Crooked developers could prey on crypto novices, claiming their app works just the same legitimate ones, and that it’s safe since it uses Libra. But if consumers get ripped off by these scammers, the anger will surely bubble up to Facebook. Even though it’s tried to distance itself sufficiently via its subsidiary Libra and the association, many people will probably always think of Libra as Facebook’s cryptocurrency and blame it for their woes.

Using Libra In The Wild

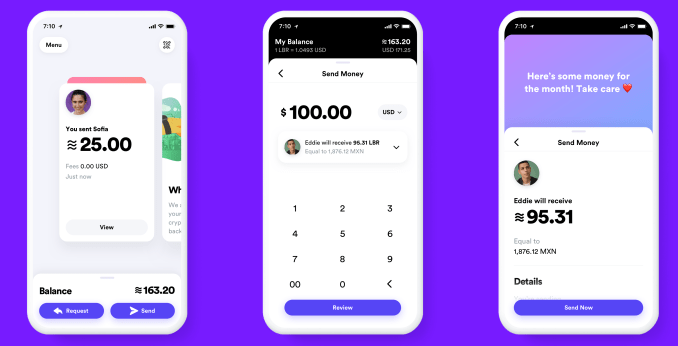

So how do you actually own and spend Libra? Through Libra wallets like Facebook’s own Calibra and others that will be built by third-parties, potentially including Libra Association members like PayPal. The idea is to make sending money to a friend or paying for something as easy as sending a Facebook Message. You won’t be able to make or receive any real payments until the official launch next year, though.

None of the Libra Association members agreed to provide details on what they’ll build on the blockchain, but we can take Facebook’s Calibra wallet as an example of the basic experience. Calibra will launch alongside the Libra currency on iOS and Android within Facebook Messenger, WhatsApp, and a standalone app. When users first sign up, they’ll be taken through a Know Your Customer anti-fraud process where they’ll have to provide a government issued photo ID and other verification info. They’ll need to conduct due diligence on customers and report suspicious activity to the authorities.

From there you’ll be able to cash in to Libra, pick a friend or merchant, set an amount to send them and add a description, and send them Libra. You’ll also be able to request Libra. It’s also likely that Calibra will offer an expedited way of paying merchants, liking scanning your or their QR code.

By default, Facebook won’t import you contact or any of your profile information but may ask if you wish to do so. It also won’t share any of your transaction data back to Facebook, so it won’t used to target you with ads, rank your News Feed, or otherwise earn Facebook money directly. Data will only be shared in specific instances in aggregated, anonymized ways or due to a request from law enforcement.

Facebook just tried to reinvent money. Next year, we’ll see if the Libra Association pulls it off.