Mozilla today announced that its Firefox Private Network (FPN), which lets you encrypt your Firefox connections, is now in an extended beta after a few months of relatively limited testing in the Firefox Test Pilot program. This beta, however, is only available to users in the U.S. and the free service is restricted to 12 hours of encrypted surfing on Firefox’s desktop version for the time being. You’ll also need a Firefox account to use the extension.

What’s maybe even more interesting, though, is that Mozilla is also working on a more fully-featured device-level VPN service that will encrypt all of your Internet surfing and app usage across your Windows 10 devices (with other platforms coming, too). This new service is now accepting invitations.

The introductory price will be $4.99 per month, making this the first service that Mozilla is directly charging users for. Those prices will likely change, though, as Mozilla learns what users are willing to pay and as it evolves the service. Given that running a VPN is costly, it definitely makes sense that the organization can’t offer it for free.

Also new today is an update to Firefox Preview, the group’s next-gen mobile browser based on its own GeckoView engine, as well as picture-in-picture support for all video sites in Firefox desktop. Firefox Preview is the publicly available test version of a new iteration of Firefox for Android. The highlight here is that Firefox Preview will now get enhanced tracking protection, similar to its desktop brethren, in addition to other new features like a new search widget for the Android home screen and a revamped Send tab for sending tabs or collections of tabs to other devices.

Salv, an anti-money laundering (AML) startup founded by former TransferWise and Skype employees, has raised $2 million in seed funding.

The round is led by Fly Ventures, alongside Passion Capital and Seedcamp. Angel investors also participating include N26 founder Maximilian Tayenthal (who seems to be doing quite a bit of angel investing), Twilio CTO Ott Kaukver, and Taavi Kotka, former CIO for Estonia (the actual country!).

Founded in June 2018 and initially offering consultancy, Estonia-based Salv has built a software platform that helps banks find and stop financial crime. The idea, says co-founder and CEO Taavi Tamkivi, is to move AML beyond just compliance to something more proactive that actually does defeat crime. That’s quite the promise, although he and his co-founders have a lot experience to draw from, both within fast-growing startups and AML.

Tamkivi built the AML, fraud, and Know Your Customer (KYC) teams at TransferWise and Skype. COO Scott McClelland also worked in the anti-fraud team at Skype, followed by a stint at TransferWise, first as an analyst and then in HR. And CTO Sergei Rumjantsev was also formerly at TransferWise, leading the engineering team responsible for KYC and verification.

“This was a highly demanding role, especially given how fast TransferWise was growing, how many new markets were coming online, and how central user verification is for compliance,” Tamkivi tells me. “Under Sergei’s leadership, the team made the verification process incredibly smooth over time for genuine customers. But also robust enough to protect TransferWise from on-boarding bad actors”.

Bad actors within financial services are aplenty, of course. Yet, despite the European banking sector spending billions tackling the problem, it is estimated that only 1-2% of global money-laundering is detected.

“AML should be all about stopping money laundering but, particularly in the last decade, layer upon layer of regulations have been added for banks to comply with,” says Tamkivi. “This would be great if that meant that there was no more money laundering, but sadly, that’s a long way off. Today, between $1-2 trillion a year is still laundered. But the excessive regulations mean that nearly all of a bank’s compliance team’s effort goes into compliance. They have very little energy left to actually focus on improving their financial crime-fighting abilities. The software they’re using is similar, focused almost wholly on compliance, not crime-fighting”.

That is where Salv wants to step in, and Tamkivi says the main difference between the startup’s AML software and other existing solutions is a much greater emphasis on crime-fighting rather than a box-ticking compliance exercise.

“We’re aiming to create a transformation similar to what’s happened in virus scanning,” he says. “10-15 years ago virus scanners on everyone’s PCs were an enormous hassle, consumed tons of resources and stopped you from getting work done. The same is true in financial institutions today. They’re using outdated, heavy software and processes to handle AML. But today, virus scanning still happens, but nobody’s worried about it. It happens in the background, with few resources. We’ll do the same in the AML world”.

In addition, the Salv CEO claims that the company’s software is faster than competitors’ offerings, both in terms of set up time and integration, and making changes to the rules the system adheres to.

“Our system, by contrast, takes a month or less to set up and minutes to modify the rules,” he says. “As a result, our customers can take everything they learn today from new criminal patterns, encode it in automated rules tomorrow, and repeat that cycle every day to protect their bank. Moving fast is the only way to keep up with the innovative organised criminals moving millions or billions around the world”.

To that end, Salv already counts Estonian bank LHV as its first customer. “They offer a full suite of banking products across Estonia,” says Tamkivi. “They’re also active in London, in particular, supporting fintechs. We have another couple of customers in the Lithuanian fintech scene. One of those is DeVere e-Money”.

More generally, Salv’s product is said to be suitable for Tier 2 and Tier 3 banks, as well as regulated fintechs and challenger banks.

Meanwhile, the business model is straightforward enough. Salv charges a monthly subscription, while the price varies based on the number of active customers a bank or fintech has.

Marvel has a trailer out for Black Widow, the story focused on the member of the Avengers team played by Scarlett Johansson. This preview of the movie features a lot of heart-pumping action, and an all-star cast that includes Rachel Weisz, Florence Pugh, David Harbour, and of course, Johansson herself.

What we get in this trailer is a look at a movie that appears to span multiple genres – it starts off looking very much like a Bourne-esque spy thriller with exciting, somewhat gritty hand-to-hand fight scenes. Later on, though, it seems to show more superhero vibes in the tradition of the big and glossy Marvel cinematic universe, though leaning more towards Captain America: Winter Soldier than the big tent circus set pieces of the core Avengers lineup, or the wacky, neon glare of the Guardians franchise and the most recent Thor.

Black Widow’s Russian spy background is clearly on display here, and it looks like there’s going to be a very weird ‘family reunion’ on display with some Russian heroes. Overall, it looks entertaining as heck – and it has a lot to live up to, as the first Marvel Studios film after Avengers: Endgame (Spider-Man: Far From Home only gets partial credit because of the shared character ownership with Sony).

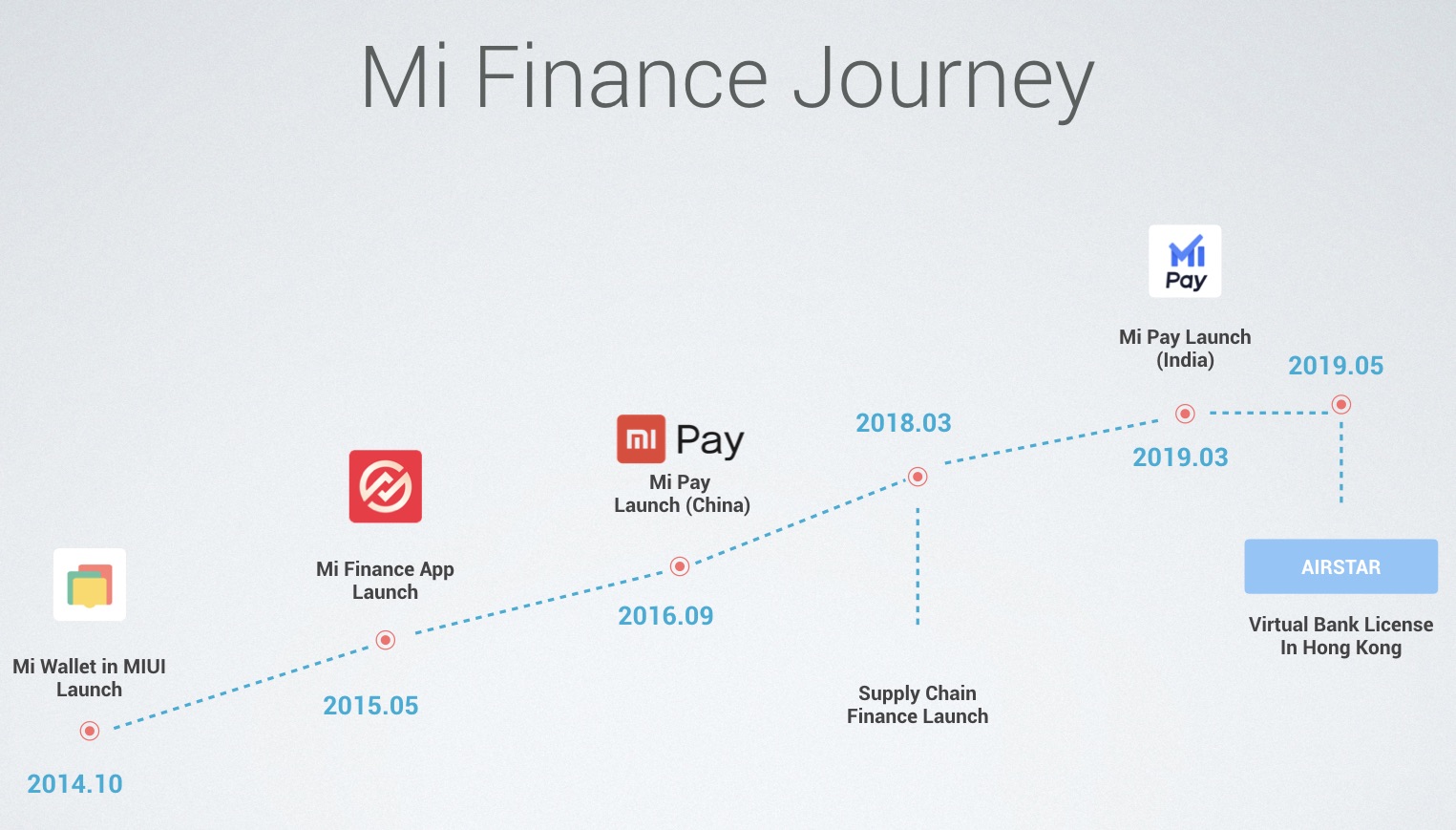

Xiaomi, the top smartphone vendor in India, today joined a growing wave of fintech startups in the nation that are offering credit to aspirational young professionals and millennials.

The Chinese electronics giant said today it is launching Mi Credit, its curated marketplace for digital lending, that offers users credit between Rs 5,000 ($70) to Rs 100,000 ($1,400).

Xiaomi said it has partnered with a number of startups such as Bangalore-based ZestMoney, CreditVidya, Money View, Aditya Birla Finance Limited, and EarlySalary to determine who should get a credit and then finance it.

Users are required to let Mi Credit app access their texts and call logs to look for transactional information and some other details to assess whether they are credit worthy. This whole process takes just a few minutes and eligible users can walk out with some credit, said Manu Jain, Vice President of Xiaomi, at a conference in New Delhi.

He added that having multiple partners for the crediting platform ensures that the likeliness of a user securing a loan is high. Once a user has secured a credit from the app, they can avail more credit in the future with a single click, the company said.

For startups that have partnered with Xiaomi, the big draw is access to a large user base, an executive with one of the partner startups said.

Xiaomi, which has been the top smartphone vendor in India for nine consecutive quarters, has an install base in tens of millions in the country. The company has shipped more than 100 million smartphones in the country, it recently revealed.

Xiaomi said the Mi Credit app will be preinstalled on all Xiaomi smartphones running Android -based MIUI operating system. The app is also available for non-Xiaomi smartphone users from the Google Play Store. (It’s not available for iPhone users.)

A wave of fintech firms have emerged in recent years in India to help millions of users secure credit and other financial services for the first time in their lives. The penetration of credit card remains very low in the country (roughly three in 100 people in India have a credit card.) This has meant that very few people in the nation have a traditional credit score.

This void has created an immense opportunity for startups to explore a range of other data points to determine who should get a loan. In emerging markets such as India, where the laws are lax, nobody appears to be alarmed with the idea of a company gleaning a lot of personal details.

As of today, Mi Credit is available to users in 1,500 zip codes, or 10 states in India. The company said it plans to extend the credit service to all of India by March next year.

Partner startups involved declined to comment on the financial arrangement they have with Xiaomi. The aforementioned unnamed executive said the agreement would vary with partners and the kind of product they are bringing to the table.

Xiaomi said it has deeply integrated its partners’ offerings into the app. As a result, users are able to see details such as disbursement of loans, lower interest, and credit score in real time.

The company began testing the app with some users in India last month. During the trial, it disbursed loans of over 280 million Indian rupees ($3.9 million).

For Xiaomi, the new offering would help it make its services ecosystem more engaging to consumers. The company, which recently posted one of its slowest growing quarterly reports, has been attempting to cut its reliance on hardware products and make more money off its internet services and through ads.

In March this year, Xiaomi launched Mi Pay, a UPI-powered payments app, in India. The company said the app has already amassed over 20 million registered users in the country.

Hong Feng, co-founder and senior vice president of Xiaomi, said the company understands the consumption behaviour of its 300 million users. “It is one of the strengths we aim to leverage to build a stronger Mi Finance business globally. We see a huge opportunity for consumer lending in India with estimations reaching up to $1 trillion dollars in digital lending by 2023, as per a report from BCG. This makes us believe that our Mi Finance business, based on solutions such as Mi Pay and Mi Credit can truly revolutionise the Indian FinTech industry.”

While French President Emmanuel Macron and U.S. President Donald Trump initially reached a deal on France’s tax on tech giants, the U.S. is moving forward with retaliation tariffs that could be as high as 100% on French goods (wine, cheese, handbags…).

The United States Trade Representative published a report following an investigation into the French tax. In a separate press release, it also recommends new tariffs and says that there could be more investigations into the digital taxes of Austria, Italy and Turkey.

“France’s Digital Services Tax (DST) discriminates against U.S. companies, is inconsistent with prevailing principles of international tax policy, and is unusually burdensome for affected U.S. companies,” the U.S. Trade Representative says.

French Finance Minister Bruno Le Maire already said on French radio that such tariffs could lead to a “strong European riposte.”

Earlier this year, France voted in favor of a new tax on tech giants. In order to avoid tax optimization schemes, big tech companies that generate significant revenue in France are taxed on their revenue generated in France.

If you’re running a company that generates more than €750 million in global revenue and €25 million in France, you have to pay 3% of your French revenue in taxes.

This tax is specifically designed for tech companies in two categories — marketplace (Amazon’s marketplace, Uber, Airbnb…) and advertising (Facebook, Google, Criteo…). While it isn’t designed to target American companies, the vast majority of big tech companies that operate in France are American.

This summer, Trump criticized France’s plans on Twitter. “France just put a digital tax on our great American technology companies. If anybody taxes them, it should be their home Country, the USA,” he wrote. “We will announce a substantial reciprocal action on Macron’s foolishness shortly. I’ve always said American wine is better than French wine!”

During the Group of Seven summit, it felt like the French government and the Trump administration found a compromise. The OECD is working on a way to properly tax tech companies in countries where they operate, with a standardized set of rules.

France promised to scrap its French tax as soon as the OECD implements its framework and pay back companies that overpaid before the OECD framework. For instance, if Facebook pays a lot of taxes in 2019 due to the French tax on tech giants and if they would have paid less under the OECD framework, France will pay back the difference.

But we’re back to square one and tariffs could jeopardize the OECD’s work.

Vancouver based mobility startup Damon Motorcycles has entered the EV arena with a preview of its first e-moto, the Hypersport Pro.

The seed-stage company had previously focused on creating digital safety technology — like its 360 degree radar detection system — to augment two-wheelers made by other manufacturers.

Damon has determined to create its own EV model designed to overcome common flaws it sees in existing motorcycle offerings.

“We are for the first time being black and white about the fact that we are a full on producer and we have a motorcycle we’re going to unveil at CES,” Damon Motorcycle founder and CEO Jay Giraud told TechCrunch.

That machine is the fully electric Damon Hypersport Pro. The news is a pre-announcement ahead of the full January debut, so Giraud would not offer much in the way of core specs — such as price, range, charge-time, and performance.

He was clear the motorcycle is meant to be a direct competitor to the latest e-motos released by Harley Davidson and California based venture Zero Motorcycles — and to the gas-motorcycle market overall.

“We’ve come at this and the motorcycle problem in a way that no other company has,” Giraud explained.

“We’re trying to change the industry by addressing the issues of safety and handling and comfort and the problems that have persisted with everyone in the industry, including all the e-moto companies today.”

Damon’s Hypersport Pro is designed around the company’s CoPilot system, which uses sensors radar and cameras to detect and track moving objects around the motorcycle, including blindspots, and alert riders to danger.

Damon has also taken on the problem of one-size fits all in motorcycle design, integrating a system on its Hypersport Pro that allows for adjustable ergonomics. The startup’s debut model will allow riders to electronically shift the motorcycle’s windscreen, seat, footpegs, and handlebars to accommodate for different positions and conditions — from more upright city riding to more aggressive high-speed runs.

Damon Motorcycles is taking pre-orders for its Hypersport Pro and will skip dealers, opting to use a direct-sales and service model similar to Tesla . The startup’s Vancouver facility is equipped to build 500 motorcycles a year, according to Giraud.

The company recently brought on Derek Dorresteyn, the former CTO of e-moto startup Alta, as its COO. Full specs of the Hypersport Pro will come next month at CES, but Giraud did offer a glimpse, saying it would be more competitive and more powerful than existing e-moto offerings.

Harley Davidson released its first e-motorcycle — the $29K LiveWire — in 2019 and California EV startup Zero Motorcycles launched its $19K SR/F, both in bids to go take e-motos mass-market. Aside from the price-gap, both have comparable charge-times (about an hour), performance, and range (around 100 miles for combined city and highway riding).

The U.S. motorcycle industry has been in pretty bad shape since the recession. New sales dropped by roughly 50% since 2008 — with sharp declines in ownership by everyone under 40 — and have never recovered.

Harley Davidon’s EV pivot is likely to bring e-moto offerings from the other large gas manufacturers, such as Honda and Yamaha, who are also attempting to revive sales to younger riders.

Harley Davidson’s LiveWire

With Damon’s pivot to e-moto production, the startup is not alone. Italy’s Energica is expanding distribution of its high-performance EVs in the U.S. Other competitors include e-moto startup Fuell, with plans to release its $10K, 150-mile range Flow in the near future.

Of course, there’s already been some speed-bumps and market attrition, with three e-moto startups — Alta Motors, Mission Motors and Brammo — forced to power down over the last several years.

So how does Damon Motors plan to succeed as a new entrant in a motorcycle market with stagnant new bikes sales and increased EV competition from established OEMs and startups?

“We have so many advantages the others don’t have and we’re leveraging everyone of their weaknesses,” founder Jay Giraud said. The company’s direct-sale model will lend to more competitive pricing and higher margins for R&D, he said.

Then there are what Damon Motorcycles sees as its Hypersport Pro’s purposely designed comparative advantages over existing manufacturers.

“You’re gonna love the horsepower and range and all that good stuff, but that’s not what makes Damon different from every one else,” explained Giraud.

“What’s different is that it’s a safer motorbike with the safety features and transforming ergonomics that will keep you from smashing into someone’s car,” he said.

Not crashing into other people’s cars is certainly a compelling feature to offer in a motorcycle. Time and sales will ultimately tell how Damon fares in the inevitable cycle of events — profitability, failure, acquisition — that will play out in the increasingly competitive e-moto space.

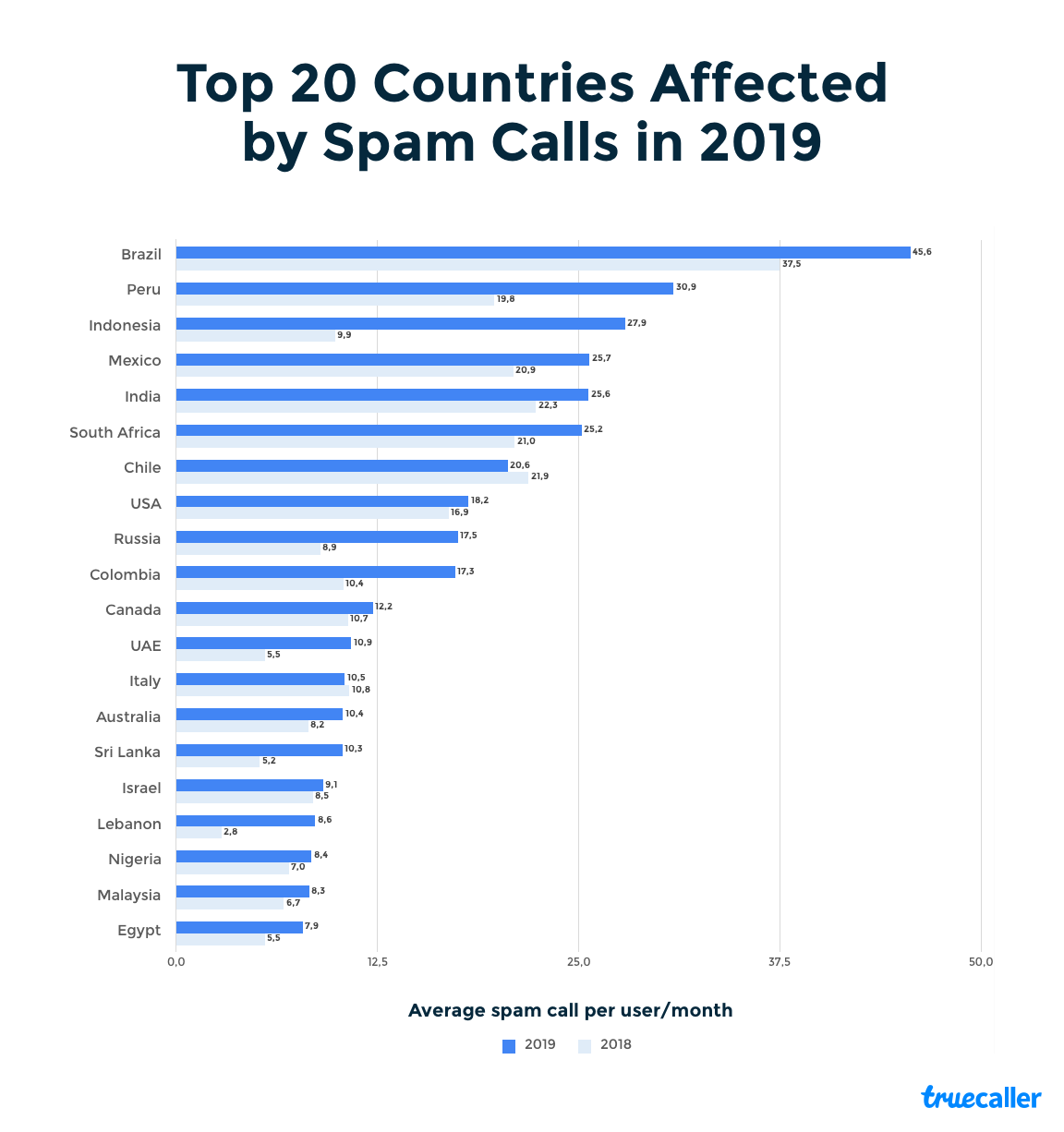

Do you feel you have been receiving more spam calls of late? You are probably not wrong — or alone.

The volume of spam calls has grown by 18% this year, according to Truecaller. In its annual report published Tuesday, the Stockholm-based firm said users received 26 billion spam calls between January and October this year — up from 17.7 billion during the same period last year.

The United States remains the eighth most spammed country, where the volume of robocalls increased by 35% this year. In a separate report earlier this year, Truecaller estimated that 43 million Americans were scammed last year and lost about $10.5 billion.

Brazil again topped the list for the most spammed country. The culprit behind the increasingly growing spam calls in the country are its own telecom operators and internet service providers. Truecaller said that in the last 12 months, calls from the operators have increased from 32% to 48%.

“These calls are typically seeking to provide special offers and upselling data plans amongst other services. Scam calls continue to be a big problem in Brazil. Two years ago, only 1% of all the top spammers were scam related, last year it went up to 20% – and this year it is up to 26%,” it said.

One of the takeaways from the report is just how complex it is to understand the nature of these spam calls. There is no common thread — or culprit — behind these calls. In some markets, such as South Africa (ranked sixth in the report), spammers are mostly making fraudulent tech support calls and conducting job offer scams.

In some other markets, like Chile (placed seventh in the report), it’s debt collectors that are placing 72% of all spam calls in the nation. In UAE, ranked 12th in the report, like Brazil, telecom operators were the ones making most of these annoying calls.

Peru, ranked second, and Indonesia, ranked third, have seen spam calls explode in the nation. In Peru, users received more than 30 spam calls in the month. Most of these calls were made by financial services that are looking to upsell credit cards and loans.

In Indonesia, spam call volume has doubled in one year. As the nation goes through tough times, scammers have tried to leverage on it, the report said. “One of the more common scams are the ‘one ring scam or Wangiri scam’. Another scam that has been going on lately is the fake hospital/injury call where someone would call and tell you that a family member or a friend is hospitalized and need immediate treatment, and you need to send them money in order for them to treat the patient.”

The position of India, where the number of mobile subscribers has ballooned from 1 million to more than a billion in two decades, is fifth on the table. It’s better than before, but spam calls are still growing in the nation. In India too, it’s the telecom operators, and then telemarketers who are together making up for more than 80% of all spam calls.

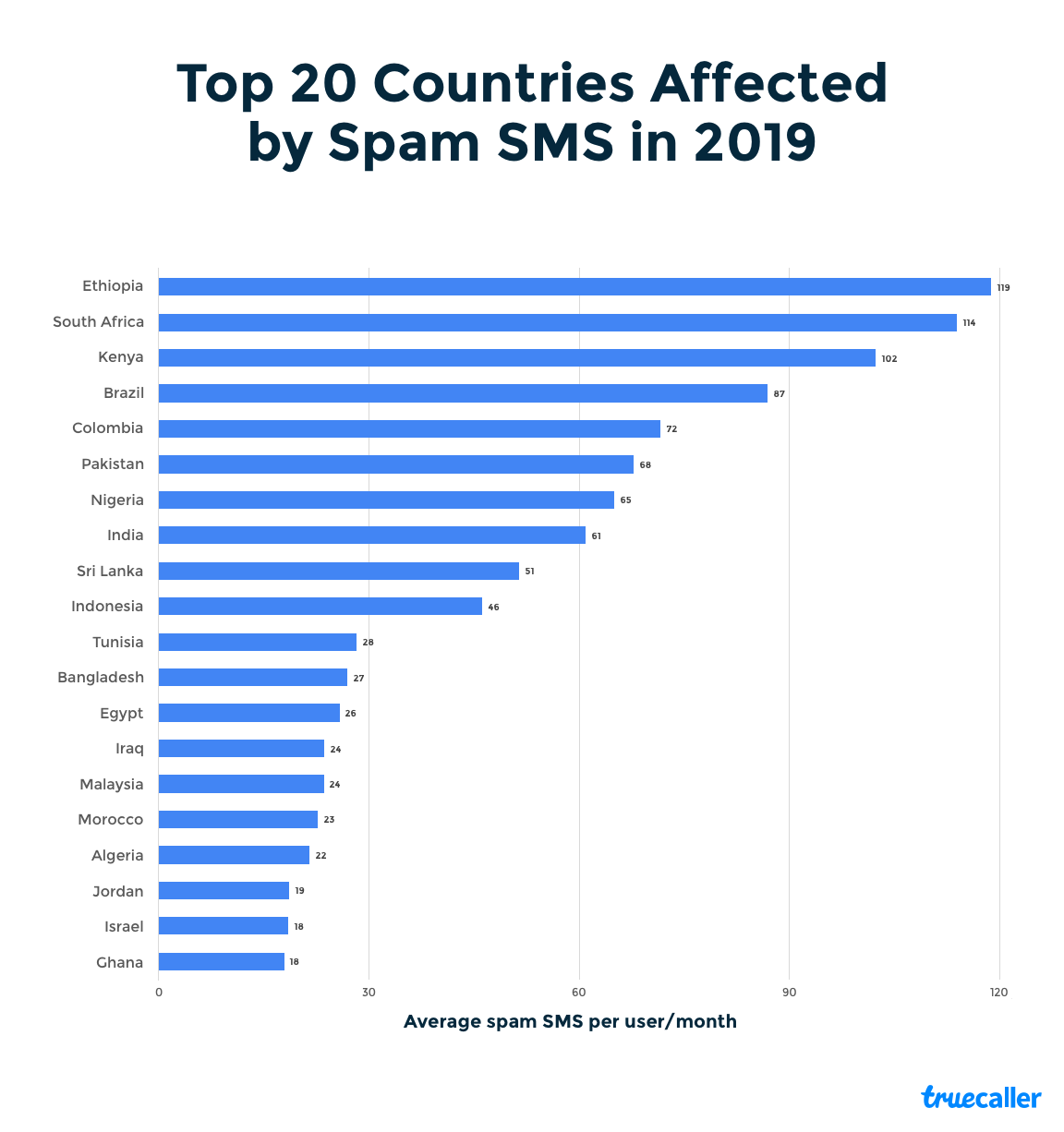

Truecaller’s report also noted that users worldwide received more than 8.6 billion spam texts this year. Below is a chart that looks at the markets that are most affected with spam SMSs.

Canadian venture capital firm Portag3 Ventures has closed a second fund focused on investing in fintech startup, with final commitments from institutional and strategic LPs totally $427 million CAD (around $320 million USD). The fund will before costing on early stage investments, and it’ll look to invest in companies globally, but with a particularly focus on Canada, the U.S., Europe and some markets in the Asia-Pacific region.

“We’re on a mission to build global champions from a Canadian base,” Portag3 CEO Adam Felesky told TechCrunch regarding the firm’s base of operations and investment targets. “Canada has the talent, the expertise and one of the biggest markets in the world directly to our south. All the ingredients are there, we just need more success stories – and we are on our way to getting them. Success will breed more success. In order to understand what it takes to succeed globally, you need to invest and work with the best of the best from around the world. Many of the early fintech unicorns are based in Europe on the back of substantive, helpful policy changes. Canada needs to learn from these examples so we get the right ingredients for building a leading, vibrant ecosystem – and we slowly but surely are.”

Contributors to this new fund include Alterna Savings and Credit Union, Aviva France, BDC Capital, Caisse de dépôt et placement du Québec, CNP Assurances, The Co-operators, Eldridge Industries, Green Shield Canada and more. The list includes a lot of strategic investors, including LPs from Portag3’s first $198 million CAD ($149 million USD) close for this fund, which was announced in October 2018.

Portag3’s Fund II has already been making investments prior to this final closing, and has already put money into KOHO, Clark, Integrate.ai and startup-builder Diagram Ventures, along with 13 other startups. Its first fund invested in a number of fintech-related companies including Clearbanc, Drop, League, and Wealthsimple, as well as some companies that have already exited including Wave, Quovo and Zensurance.

Alongside the close of this funding, Portag3 has also recently set up a new group of senior advisors to work with the companies it’s investing in, and those advisors include financial industry heavyweights like Rockefeller Capital Management CEO and president Gregory J. Fleming, as well as former AIG president and CEO Peter Hancock.

Exact terms of the deal remain undisclosed, although the exit sees at least some of Shift’s investors, such as Cherry Ventures, picking up shares in Xometry . I also understand the Shift team is staying on and the company’s founders, Albert Belousov, Dmitry Kafidov and Alexander Belskiy, will now be heading up Xometry’s newly formed European business.

Specifically, via this acquisition, Xometry says will accelerate international expansion into 12 new countries, leveraging a now worldwide network of over 4,000 manufacturers. The company’s on-demand manufacturing marketplace is already used by global companies like BMW and Bosch, which are Europe-based, and so it makes sense to have a much stronger operations in the continent.

“We’re eager to leverage Xometry’s technology to continue to scale our business in Europe,” says Shift’s Kafidov in a statement. “We look forward to providing our customers additional manufacturing capabilities, including additive manufacturing and injection molding”.

Shift claims to have built the largest on-demand manufacturing network in Europe and a customer base that includes some of the leading manufacturing companies in the region. Now operating as Xometry Europe, the subsidiary will continue to be headquartered in Munich in Germany, an area known for its manufacturing heritage.

Cue statement from Christian Meermann, Founding Partner, Cherry Ventures: “The custom manufacturing industry is a massive global market of over $100 billion. We’re excited for Shift to utilize Xometry’s industry-leading technology as well as leverage the global manufacturing expertise from other Xometry investors, including BMW i Ventures and Robert Bosch Venture Capital”.

Xometry has raised $118 million since being founded in 2013. Over the past two years, the company has grown from 100 employees to over 300 while more than doubling revenue each year. Via its partner manufacturing facilities, the company offers CNC Machining, 3D Printing, Sheet Metal Fabrication, Injection Molding, and Urethane Casting.

Contrast that with Shift, which was founded in 2018 and had raised around €4 million (~$4.4m) to date. Sources also tell me that the startup had nearly closed a Series A round before Xometry preempted the investment by making an acquisition offer.

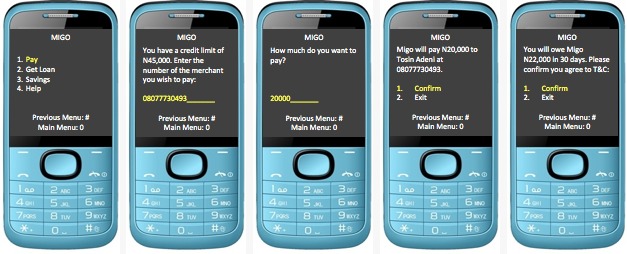

After growing its lending business in West Africa, emerging markets credit startup Migo is expanding to Brazil on a $20 million Series B funding round led by Valor Group Capital.

The San Mateo based company — previously branded Mines.io — provides AI driven products to large firms so those companies can extend credit to underbanked consumers in viable ways.

That generally means making lending services to low-income populations in emerging markets profitable for big corporates, where they previously were not.

Founded in 2013, Migo launched in Nigeria, where the startup now counts fintech unicorn Interswitch and Africa’s largest telecom, MTN, among its clients.

Offering its branded products through partner channels, Migo has originated over 3 million loans to over 1 million customers in Nigeria since 2017, according to company stats.

“The global social inequality challenge is driven by a lack of access to credit. If you look at the middle class in developed countries, it is largely built on access to credit,” Migo founder and CEO Ekechi Nwokah told TechCrunch.

“What we are trying to do is to make prosperity available to all by reinventing the way people access and use credit,” he explained.

Migo does this through its cloud-based, data-driven platform to help banks, companies, and telcos make credit decisions around populations they previously may have bypassed.

These entities integrate Migo’s API into their apps to offer these overlooked market segments digital accounts and lines of credit, Nwokah explained.

“Many people are trying to do this with small micro-loans. That’s the first place you understand risk, but we’re developing into point of sale solutions,” he said.

Migo’s client consumers can access their credit-lines and make payments by entering a merchant phone number on their phone (via USSD) and then clicking on “Pay with Migo”. Migo can also be set up for use with QR codes, according to Nwokah.

He believes structural factors in frontier and emerging markets make it difficult for large institutions to serve people without traditional credit profiles.

“What makes it hard for the banks is its just too expensive,” he said of establishing the infrastructure, technology, and staff to serve these market segments.

Nwokah sees similarities in unbanked and underbanked populations across the world, including Brazil and African countries such as Nigeria.

“Statistically, the number of people without credit in Nigeria is about 90 million people and its about 100 million adults that don’t have access to credit in Brazil. The countries are roughly the same size and the problem is roughly the same,” he said.

On clients in Brazil, Migo has a number of deals in the pipeline — according to Nwokah — and has signed a deal with a big-name partner in the South American country of 290 million, but could not yet disclose which one.

Migo generates revenue through interest and fees on its products. With lead investor Valor Group Capital, new investors Africinvest and Cathay Innovation joined existing backers Velocity Capital and The Rise Fund on the startup’s $20 million Series B.

Increasingly, Africa — with its large share of the world’s unbanked — and Nigeria — home to the continent’s largest economy and population — have become proving grounds for startups looking to create scalable emerging market finance solutions.

Migo could become a pioneer of sorts by shaping a fintech credit product in Africa with application in frontier, emerging, and developed markets.

“We could actually take this to the U.S. We’ve had discussions with several partners about bringing the the technology to the U.S. and Europe,” said founder Ekechi Nwokah. In the near-term, though, Migo is more likely to expand to Asia, he said.

The introductory price will be $4.99 per month, making this the first service that Mozilla is directly charging users for. Those prices will likely change, though, as Mozilla learns what users are willing to pay and as it evolves the service. Given that running a VPN is costly, it definitely makes sense that the organization can’t offer it for free.

The introductory price will be $4.99 per month, making this the first service that Mozilla is directly charging users for. Those prices will likely change, though, as Mozilla learns what users are willing to pay and as it evolves the service. Given that running a VPN is costly, it definitely makes sense that the organization can’t offer it for free.

The company recently brought on Derek Dorresteyn, the former CTO of e-moto startup Alta, as its COO. Full specs of the Hypersport Pro will come next month at CES, but Giraud did offer a glimpse, saying it would be more competitive and more powerful than existing e-moto offerings.

The company recently brought on Derek Dorresteyn, the former CTO of e-moto startup Alta, as its COO. Full specs of the Hypersport Pro will come next month at CES, but Giraud did offer a glimpse, saying it would be more competitive and more powerful than existing e-moto offerings.