So much for Walmart’s big and expensive effort to take on Amazon with a digitally-native brand. Today, the retail giant announced in its quarterly report that it would be discontinuing Jet.com, the online-only marketplace that it acquired for $3 billion when it was just over one year old.

“Due to continued strength of the Walmart.com brand, the company will discontinue Jet.com,” the company said in a short statement. “The acquisition of Jet.com nearly four years ago was critical to accelerating our omni strategy.”

The company also reported earnings that saw growth of less than 10% in its core US market, and the company withdrawing guidance for fiscal 2021.

“The company’s net sales and operating results were significantly affected by the outbreak of COVID-19,” Walmart said. “Unprecedented demand for products across multiple categories led to strong top-line results. Certain incremental costs negatively affected operating income, including costs associated with enhanced wages and benefits as well as safety and sanitation.” Total revenue was $134.6 billion, an increase of $10.7 billion, or 8.6%.

Although the COVID-19 pandemic has led to a surge of people shopping online, a number of companies, including Amazon and eBay have found that handling business at the moment can prove to come with more overhead costs, and that’s before considering what the larger effects of a collapsed economy will have on overall sales. So while it might seem counterintuitive to get rid of Jet.com at a time like this, it’s about cost cutting ultimately because of that bigger picture.

When Walmart acquired Jet.com in 2016, the big ambition was to give the giant retailer a complement to its brick-and-mortar stores to compete better against Amazon and its growing presence as a primary shopping destination. Buying Jet.com was also about bringing on its experienced founder and leader Marc Lore to lead both Jet and Walmart online

“This is Walmart being even more committed to winning in e-commerce,” said Doug McMillon, president and CEO of Walmart, in a conference call with investors at the time.

But fast forward to today, amid all the strains that COVID-19 is putting on the retail sector and the wider economy, and the discontinuation is the final chapter in what ultimately was a problematic endeavour for the company that it tried to restructure to make more effective. That included, last year, fully integrating Jet’s teams into its own, while still keeping the brand; and also axing various Jet experiments like Jet Black, a personal shopping service.

In the meantime, it’s been working on adding more Walmart.com perks such as piloting a two-hour deliver service at the end of last month.

The acute pain of California’s housing crisis can be measured in the human toll it takes on the increasing numbers of families made homeless by rising rents and the billions of dollars the state loses to the high cost of living.

After wrestling with recalcitrant homeowners, husbanding their parcels of land to keep their property values high, the state’s leadership passed a law that increased the availability of new rental units and put more money into homeowners’ pockets in 2016. The passage of the law has unlocked a wave of entrepreneurial energy as startups look to build things that can make money and solve a real problem for the state — and eventually — the nation.

These companies aren’t building new gaming platforms or cryptocurrency applications, but instead are trying to find ways to bring low-cost housing at an affordable price to homeowners who could use the additional income and renters who are spending increasingly more money for increasingly smaller spaces — if they can afford those homes at all.

“What was important to me was creating affordable housing,” said United Dwelling founder and chief executive Steven Dietz. A former venture capitalist and the co-founder of the firm that would become Los Angeles’ largest, Upfront Ventures, Dietz decided to start his company as a response to what he sees as the largest problem that California faces.

The problem with other companies building pre-fabricated or modular homes for what are called accessory dwelling units on California properties is that they’re not being built for middle-class homeowners.

“Homeowners have this valuable property which is an attached two-car garage,” said Dietz. “We go to the homeowner and say you have this property here. You can put in a small home and rent it out and it will be a source of income to you.”

Homeowners can either lease the studio home to United Dwelling and receive a few hundred dollars a month for the property, or buy out the company for $87,900 and have United Dwelling manage the property. The Culver City, Calif.-based company makes money on the sale of the house, managing the rental and connecting homeowners to a lender that will give them money to acquire the rental property.

That bid was enough to convince Davita and Martin Macauley, a couple who own a home in Los Angeles’ Gramercy Park neighborhood and are two of United Dwelling’s first customers. “Garage conversions were a new concept for us,” Martin McCauley told Curbed Los Angeles. “But it made sense when you think about the amount of people who have garages, and if we got all of that junk out of our garage, we’d actually have about five things we actually need.”

There are over 831,000 homes in Los Angeles that meet the criteria for United Dwelling’s construction, which amounts to a 20 foot by 24 foot space.

“The original plan was to remodel existing garage,” Dietz said, “but after we did two of them and put a bunch more through the permitting process we realized remodeling a 70 year old structure built as a garage and turning it into a home was not scalable.”

Instead, Dietz and the architecture firm Modative collaborated on a new design for a pre-fabricated house. The United Dwelling houses are equipped with the latest appliances and their insulation and electrical ranges, washers, and dryers mean that the apartments have net zero energy consumption and a net zero carbon footprint, according to Dietz.

Modative isn’t the only partner from the Los Angeles community that United Dwelling has brought on board. The company uses a local nonprofit organization called Chrysalis to build its units. The nonprofit is designed to help low-income individuals find employment and get on the path to economic self-sufficiency, according to the company.

According to an October article in The New York Times, the rent for one of United Dwelling’s detached studio apartments around the University of Southern California’s campus would cost roughly $1400 per month. The prices will vary by neighborhood, but Dietz expects them to run 20 percent less than the average cost of an apartment in the same neighborhood, he said.

Since that article’s publication, the timing for Dietz’s planned roll out of several hundred homes stalled and the investor turned entrepreneur, who had previously financed the company himself, went out to raise cash from venture investors.

The term sheets for the round came in at the end of February, and then the pandemic hit. Rather than wait for his investors to call him, Dietz approached Lightspeed and Alpha Edison, which led the round, about changing the terms of the deal. “[I] changed the price by 11 percent and walked that through and continued to move forward,” Dietz said.

There are currently five homeowners who have agreed to be guinea pigs for the United Dwelling experiment in urban reconfiguration, but Dietz said that the company would have 150 buildings under management by the end of the year, and 1700 by the end of 2021.

For Nick Grouf, the founder of Alpha Edison, it was both Dietz’s experience as an investor and the company’s vision for the future that compelled the firm to commit capital.

“We’ve been spending a lot of time thinking about fundamental social challenges,” said Grouf. “And an area that has been causing an incredible amount of pain is affordable housing. [And] one of the areas where we have been spending a lot of time is trying to find a business that we felt had real scalability and that really represented innovation and where we had confidence that there would be durable growth.”

One of the lynchpins that sealed the deal was the as-yet-undisclosed partnership with a lender who could help move the needle on getting homeowners to build. “This is not an inexpensive decision although it is an economically compelling decision,” said Grouf. “From a cash flow perspective, it is not only creating a more valuable asset for the homeowner and creating revenue streams that they have historically not had… there is this latent supply of outbuildings that can be converted into usable housing. When you can match that latent supply with latent demand. Where people would love to live in some of these neighborhoods.. What Steven has done in unlock that supply and demand in a way that’s economically compelling.”

As the coronavirus pandemic continues, throwing countries into lockdown and recession, two of the hardest-hit sectors have been travel and events. And startups operating in the space that have recently raised significant funding aren’t immune to the crisis.

Pollen, the U.K.-based influencer marketplace for travel and events that closed $60 million in funding in October, has axed about 31% of its staff, nearly 70 people, across the US and Canada, TechCrunch has learned. In addition, multiple sources, who spoke on the condition of anonymity, say that around three dozen staff in the U.K. have been put on furlough and that up to 10 U.K. contractors have been let go.

Founded in 2014 and previously called Verve, Pollen operates in the influencer or “word-of-mouth” marketing space. The marketplace lets friends or “members” discover and book travel, events and other experiences — and in turn helps promoters use word-of-mouth recommendations to sell tickets. Pollen’s backers include Northzone, Sienna Capital, Draper Esprit, Backed and Kindred.

Confirming the North American job cuts, Pollen co-founder and CEO Callum Negus-Fancey (pictured right) told TechCrunch that 24 team members in Las Vegas have been axed, 29 in LA, 6 in Canada, and 10 that worked remote throughout U.S. That’s a cull of approximately 31% of Pollen’s 216 staff overall.

He also said that around 34 U.K. employees have been furloughed, and confirmed that the furloughed staff in question are being paid 80% of their salary up to £2,500 (via the U.K. taxpayer), with no top up from Pollen.

We also understand from sources that U.S. staff were provided with no additional severance, and that some staff were given as little as one week’s notice. Negus-Fancey doesn’t entirely dispute this, telling TechCrunch that “U.S. employees were given 1 week severance, plus 1 week for each additional year they [were] with the company” rounded up to the nearest 12 months.

The Pollen CEO also confirmed that U.S. employees were not given any paid additional medical benefits beyond the month they were served notice. However, each staff member laid off has the option to continue with COBRA coverage at their own cost.

Meanwhile, back in the U.K., a picture of confusion has emerged with regards to whether or not all U.K. staff put on furlough under the Coronavirus Job Retention Scheme will have jobs to return to.

Internal communication seen by TechCrunch shows Pollen management in late March discussing plans to make a group of U.K. staff redundant and then ask them to go on furlough in the interim anyway i.e. in a number of instances there wouldn’t be a job being retained.

Some days later, a series of group Zoom calls, rather than one-to-ones, were held between managers and teams affected. Accounts of exactly what was discussed on those calls vary, although some people present said attendees were “shocked,” with one attendee describing the atmosphere as “uncomfortable”.

Emails subsequently sent from team managers to a number of individual team members appear to offer confirmation that they no longer had a role at the company but would be offered furlough from 1st of April onwards. Those staff were also locked out of Pollen’s systems with immediate effect (Slack, emails etc.), and in some instances offered “next steps” coaching and help with job search.

Separate emails sent to affected staff by Pollen’s General Counsel sought “deemed consent” in relation to being put on furlough, giving them just 24 hours to raise any objections.

Asked about internal discussions with regards to redundancies and staff being told by their managers that they were being let go, Negus-Fancey disputes that U.K. staff put on furlough no longer have jobs to return to. In a statement provided to TechCrunch he said “there is a possibility for every employee who has been put on furlough to have their job back”.

Adds the Pollen CEO:

We believed it was appropriate to tell some employees it was unlikely they would get their job back – this seemed like the humane and appropriate thing to do. There was so much uncertainty at the time and we were processing/managing unknown territory and a lot of new information. We had no way of knowing the answer to the question and did not want to mislead anyone or give them a false sense of hope. This made sure that affected employees fully understood the situation and could plan accordingly. Some have looked for new permanent roles and successfully found a new role and we are happy for them. Our number one goal was to put our team first and support them during this time.

The scheme has been very successful, many employees who would have otherwise been made redundant will now keep their job. The extension of the scheme has further increased the number of jobs which will be saved at Pollen.

Furthermore, Negus-Fancey says “FAQs and other resources” were produced to help managers with furlough conversations, adding that if any management “miscommunicated” to U.K. staff that they were being let go, then this “would have been because of a misunderstanding”.

One question the Pollen founder wasn’t able to answer immediately was why some furloughed employees had access to the company’s systems revoked, while others did not, if they were all expected to return to work once the furlough period ended.

Initially, Negus-Fancey suggested it was so that furloughed staff wouldn’t be tempted to work (under the Coronavirus Job Retention Scheme, working for the company that put you on furlough is prohibited).

Later, after clarifying this with members of his U.K. team, he emailed to say that “employees who were furloughed who had the highest possibility of coming back (top of the list if jobs became available) were not locked out of some systems e.g. social tools. On top of this, anyone who asked not to be locked out, wasn’t locked out”.

Travel and events at a standstill

The upheaval at Pollen is just one example of the challenges that travel and events-focused tech companies have faced in recent weeks. With consumers virtually unable to travel anywhere or converge for any in-person group events, companies that have built business models around such leisure activities have found themselves scrambling to reduce their burn rate or having to more fundamentally change how they operate.

Airbnb is probably the most high-profile example. The popular peer-to-peer accommodation and experiences platform has seen a halt to much of its business in the last two months, leading it to lay off 1,900 employees (25% of its global workforce) and rethink its product offerings. It’s also seen its valuation nearly halved to $18 billion according to reports. Another example is TripAdvisor, which announced it was laying off 900 people, or 25% of staff.

In the case of event-based companies (events being a key part of Pollen’s business model), there is an argument to be made that even before the coronavirus took hold, it was a challenging business model for all but the most focused and scaled efforts.

Fyre Festival, with its own focus on exclusivity and influencer marketing, was an infamous flop; the U.K.’s Yplan eventually sold at a major loss, and Eventbrite, which is now public, has seen its stock drop drastically since mid-February, just as COVID-19 really started to take its grip on the globe. It’s not all doom and gloom — pre-coronavirus crisis, Get Your Guide had actually been scaling nicely — but it’s a grim situation.

Turning back to Pollen, the company says that even with the coronavirus crisis, it has been bringing in revenue by shifting to selling experiences for 2021. Asked about current burn-rate, post-layoffs, Negus-Fancey said Pollen does not disclose its cash position publicly. “However, we’re comfortable from a financial perspective,” he added.

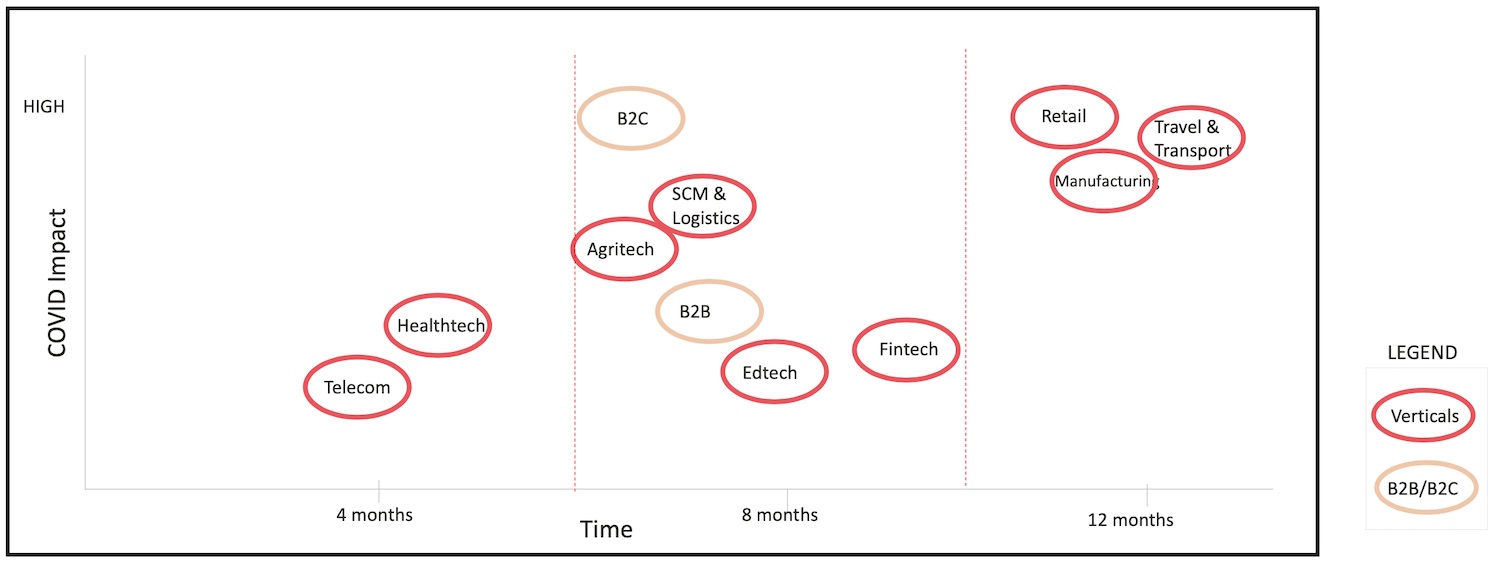

More than two-thirds of startups in India need to secure additional capital in the coming weeks to steer through the coronavirus pandemic, according to an industry report.

70% of startups in India, home to one of the world’s largest startup ecosystems, have less than three months of cash runway in the bank, and another 22% have enough to barely make it to the end of the year, according to a survey conducted by industry body Nasscom.

Only 8% of startups that participated in Nasscom’s survey said they had enough money to survive for more than nine months, the report published on Tuesday said.

As startups confront unprecedented times, many are thinking of taking dramatic steps to stay afloat. About 54% of some 250 respondents said they were looking to pivot to new business opportunities, and 40% said they wanted to diversify into growth verticals such as healthcare.

For some startups, there are other factors at play, too. More than 69% of business-to-business startups, especially those operating in retail and fintech categories, say in the report that they are facing delays in payments from their clients.

This has left more than 50% of such startups to enforce pay cuts, reduction in marketing spends, and a quarter of them to switch to a lower-cost vendor to save money.

Startups operating in transport and travel sectors are also severely impacted, with 78% of respondents saying they were rethinking their business models and tweaking their products in accordance with the current scenario.

In a call with reporters on Tuesday, executives at Oyo unveiled new steps the budget lodging startup had taken at its hotels to ensure safety for operators and customers. They also said they were hoping that the government would allow more people to travel and stay at hotels again.

More than two-thirds of startups said they were looking for policies that eased regulations and spur government purchases. Many also requested relief in taxations for a few years.

More than two-thirds of Indian startups believe the impact of coronavirus will linger for up to 12 months. (Nasscom)

Earlier this month, India announced a $266 billion stimulus package to help revive the stalled economy. On Saturday, Indian Finance Minister Nirmala Sitharaman said that startups too will be able to access some of this relief — though details remain sparse on how they should go about it.

Since 2017, India’s startup ecosystem has grown consistently. Last year, startups in the country raised a record $14.5 billion.

“Out of the blue, this flourishing growth saga has suddenly been hit by a roadblock… the COVID roadblock. There is no country, business or living being that has not been affected by the COVID pandemic. While governments have been working diligently to protect and save human lives, businesses have been hit and small businesses and start-ups have been the most affected,” said Debjani Ghosh, President of NASSCOM, in the report.

Adedana Ashebir is regional manager for Africa for Village Capital, which has supported more than 100 entrepreneurs and 15 entrepreneur support organizations in Sub-Saharan Africa since 2012.

As the fallout from COVID-19 continues to grip Africa’s major economies, the tech ventures in those countries need state support.

National legislation that creates clear frameworks and operational support for startups are one of the best ways to help Africa’s digital companies survive and thrive through the coronavirus crisis — and improve their environment over the long term.

Africa has dozens of thriving startup ecosystems that are persevering through this crisis, but now more than ever, they need a boost. The gains made by founders thus far are in danger due to the ongoing economic slowdown. The World Bank estimates that economic growth in sub-Saharan Africa alone will decline from 2.4% last year to -2.1 to -5.1% this year. If correct, the region will experience its first recession in a quarter of a century.

Now is the time for something that was already long-overdue in many African countries: political leaders should support startups through national startup acts.

Village Capital’s Adedana Ashebir, Image Credits: Village Capital

Last December, Senegal became the second African nation to enact a national Startup Act, following Tunisia’s landmark bill that passed in April 2018. Other countries may follow soon: startup legislation was being discussed in Ghana and Mali before the novel coronavirus monopolized headlines.

The rest of the continent can learn a lot from Tunisia, which passed its Startup Act in 2018 after receiving input from entrepreneurs and economists. In addition to clarifying rules surrounding angel, seed and venture capital funding, the act bestows benefits on companies designated as startups. This includes alleviating their tax and social security contribution burdens, providing access to forex bank accounts and offering subsidized salaries for founders. More than 50 startups have taken advantage of the “startup” label. A number of Tunisian entrepreneurs have told me that thanks to the new legislation, they are able reinvest savings from these incentives back into their businesses.

TikTok’s parent company ByteDance has added Lingxi, a Beijing-based startup that applies machine intelligence to financial services such as debt collection and insurance sales, to its ever-expanding portfolio of investments.

The AI startup has raised a $6.2 million Series A round co-led by ByteDance and Rocket Internet, the German accelerator that has incubated e-commerce giants Lazada and Jumia. Junsan Capital and GSR Ventures also participated in the round, which officially closed in April.

This marks one of ByteDance’s first investment deals for purely monetary returns, rather than for an immediate strategic purpose. However, with ByteDance’s recent foray into the financial services domain, that relationship could shift over time.

ByteDance as an investor

TikTok’s parent company previously focused narrowly on strategic deals, with the aim of leveraging these smaller startups’ technology, industry know-how, talents and other resources for its own business objectives. The most prominent example is perhaps its acquisition of Musical.ly, through which TikTok gained access to tens of millions of American users and a reputed product team led by founder Alex Zhu.

In 2019, ByteDance’s strategic investment team began its search for venture capital-style funding opportunities. Spearheading the effort is former Sequoia China investor Yang Jie.

There are, however, clear strategic synergies in ByteDance’s first financial investment. The online entertainment giant has already received an insurance broker license and is in the process of obtaining one for consumer finance, according to Lingxi founder and chief executive Zhongpu “Vincent” Xia. When asked if he sees ByteDance eventually deploying Lingxi’s machine intelligence in its future financial services, Xia responded, “Why not?”

ByteDance declined to comment on its entry into the financial sector.

Despite billing themselves as AI-first companies, both ByteDance and Lingxi recognize the essential role of humans before AI reaches the desired level of sophistication. ByteDance today relies on thousands of human auditors to screen content published across its TikTok, Douyin, Today’s Headlines and other apps. Likewise, Lingxi is labor-intensive and manages 200 customer representatives aided by a team of 30 AI experts.

The core of Lingxi is to “augment humans, not to replace them,” said Xia in a phone interview with TechCrunch .

Too big to change

Xia was leading a team of 90 people to work on Baidu’s commercialization of AI when he had an epiphany to do something of his own. He was convinced that AI would enhance humans’ cognitive capability, he said, the same way the steam engine had boosted humans’ physical production a century ago. The Chinese search pioneer has widely been perceived as the poster child of the nation’s booming AI industry because of its early and outsized investment in the technology, but by the end of 2017, Xia felt Baidu’s model of touting AI as a tool wasn’t working.

“We hit a bottleneck. The technology [AI] wasn’t mature enough yet, which means you have to combine it with a big team of people to perform manual tasks like data labeling, so you not only need to hire AI experts, professionals in the business you serve, but also a large number of workers to label data and train the machines,” he said.

Xia is among the industry practitioners who recognize the limitation of machines. While computers can outperform humans in completing repetitive, menial tasks, they remain unreliable in handling complex human emotions and can lead to counterproductive and even detrimental repercussions were they left with full autonomy.

The result of relying completely on machines is “client dissatisfaction,” said Xia. “The client might be very happy for the first few months, but as its business evolves and new needs arise, it will start to realize that the so-called machines are getting dumber and dumber. Artificial intelligence becomes artificial retardedness.”

Lingxi staff at work during the COVID-19 pandemic

Most self-proclaimed AI startups in China make money by selling bots akin to how old-fashioned software was sold with pre-programmed objectives, allowing little room for iteration or upgrade later on. Lingxi, in contrast, is service-based and takes a commission from client revenues.

Take debt collection — Lingxi’s primary focus at this stage — for example. When a client, a financial affiliate of one of China’s biggest internet firms, assigned Lingxi with 1.9 million yuan (about $270,000) worth of debt, the startup’s algorithms first determined how much the machines could handle. It turned out that the robots recovered 1.7 million yuan and left the rest of the cases, which Xia categorized as “irrational and complicated,” to human staff. By Q1 2020, Lingxi was able to achieve 2.5 times the average output of debt collection agencies, and it aims to ramp up the ratio to 4 times by the end of the year.

Human control

Conventionally, a company selling AI tools deals only with the IT department from its clients. Lingxi works with the business department instead. In the client’s eye, the AI startup is no different from a traditional debt collector. In practice, Lingxi is a debt collector with souped-up productivity enabled by computing power.

“The client doesn’t care what tools we use. They care only about the result,” said Xia. “The difference in working with these two departments is that the one in charge of the actual business is result-driven and will give us much stricter KPIs.”

The immediate impact of this model is that the AI-driven vendor must keep improving its algorithms, manually sampling and correcting machine decisions to improve their accuracy. “We might not be making money in the beginning, but over time, our output will certainly surpass those of our competitors.”

The service-oriented approach pushes Lingxi to get its hands dirty, upending the image of tech startups coding away in their sleek and comfortable offices. Its engineers are asked to regularly talk to clients about their real-life business challenges, whereas its customer representatives are required to attend training in how AI works.

“Fusion is what defines our company culture,” said Xia introspectively. “The technical team needs to understand business practices. Vice versa, our business people need to understand technology.”

Coveted sector

It’s not hard to see why Xia chose to target China’s financial services industry. The booming sector is lucrative and tends to be more progressive in embracing technological innovations. Competition in fintech runs high, leveling the playing field for newer entrants against those that are more established.

“There’s a saying in the Chinese tech world that goes: If you can conquer the financial industry, you have conquered the business-to-business world,” said the founder.

The three-year-old startup is targeting 40-80 million yuan ($5.6 million to $11.3 million) in revenue in 2020. It’s one of the few businesses that have, against the odds, thrived under the COVID-19 pandemic because more people are taking out loans to tide the looming economic downturn.

Meanwhile, traditional debt collectors are struggling to hire during city lockdowns due to travel bans across the country, which started to ease in March, while machine-only vendors still fail to satisfy the whole range of client demands. That gave Lingxi a big window to onboard a significant number of new clients, prompting it to hire new staff.

Entrepreneur First (EF), the London-headquartered “talent investor” that backs individuals pre-team and pre-idea to enable them to found startups, has appointed former Andreessen Horowitz partner Benedict Evans as a Venture Partner.

A well-respected analyst with a background in the tech and media industries, Evans will be tasked with providing “analysis, insight and recommendations” for new technologies and markets that offer opportunities for the EF company builder model and to support future EF cohorts.

This will include acting as an advisor to EF’s global portfolio, and supporting the current and upcoming cohorts at Investment Committee. Additionally, I’m told he’ll be working with EF’s Executive Committee on “strategy and portfolio composition direction” (whatever that means!).

Noteworthy, Evans’ LinkedIn profile lists him as a Venture Partner at London’s Mosaic Ventures. Mosaic primarily invests at Series A, and therefore further along the funding funnel than EF. Presumably, that means there is no direct conflict of interest and I understand he’ll continue to do around one day per week at Mosaic.

(Fun fact: all the way back in late 2013, Evans did a stint at seed investment firm Passion Capital based in London. The “analyst in residence” left after 3-4 months and intriguingly that part of his resume doesn’t get the LinkedIn treatment.)

Meanwhile, for the last six years, Evans was based in San Francisco where he was a partner at Andreessen Horowitz. Upon leaving Andreessen Horowitz, he returned to London as an independent analyst, continuing to produce annual macro tech trends reports, as well as producing a regular newsletter.

Alongside Evans, EF has recently recruited Sam Barnett as President, Bernadette Cho as General Manager of EF Singapore, Philipp Herkelmann as General Manager of EF Berlin, and Andy Young as Vice President of Growth.

Arculus, the Ingolstadt, Germany-based startup that has developed a “modular production platform” to bring assembly lines into the 21st century, has raised €16 million in Series A investment.

Leading the round is European venture firm Atomico, with participation from Visionaries Club and previous investor La Famiglia. Arculus says it will use the injection of capital to “strengthen product development, broaden customer base and prepare for a global rollout”.

As part of the investment, Atomico partner Siraj Khaliq is joining the Arculus board. (Khaliq seems to be on a bit of a run at the moment after quietly leading the firm’s investment in quantum computing company PsiQuantum last month.)

Founded in 2016, Arculus already works with some of the leading manufacturing companies across a range of industries. They include Siemens in robotics, heating, ventilation and air conditioning, Viessmann in logistics, and Audi in automotive.

Its self-described mission is to transform the “one-dimensional” assembly line of the 20th century into a more flexible modular production process that is capable of manufacturing today’s most complex products in a much more efficient way.

Instead of a single line with a conveyor belt, a factory powered by Arculus’ hardware and software is made up of modules in which individual tasks are performed and the company’s robots — dubbed “arculees” — move objects between these modules automatically based on which stations are free at that moment. Underlying this system is the assembly priority chart, a tree of interdependencies that connects all the processes needed to complete individual products.

That’s in contrast to more traditional linear manufacturing, which, claims Arculus, hasn’t been able to keep up as demand for customisation increases and “innovation cycles speed up”.

Explains Fabian Rusitschka, co-founder and CEO of Arculus: “Manufacturers can hardly predict what their customers will demand in the future, but they need to invest in production systems designed for specific outputs that will last for years. With Modular Production we can now ensure optimal productivity for our customers, whatever the volume or mix. This technological shift in manufacturing, from linear to bespoke, has been long overdue but for manufacturers looking ahead at the coming decades of shifting consumer buying behaviours it is mission critical to survival”.

To that end, Arculus is making some bold claims, namely that the company’s technology increases worker productivity by 30% and reduces space consumption by 20%. It also reckons it can save its customers up to €155 million per plant every year “at full implementation”.

Siraj Khaliq, Partner at Atomico, says the manufacturing sector “is huge and the inefficiencies are well known”.

“We estimate that the auto industry alone could save nearly $100bn, were all manufacturers to adopt Arculus’s modular production technology,” he tells TechCrunch. “And beyond auto, their technology applies to any linear/assembly line manufacturing process – in time perhaps a tenfold greater market still. We’ve already seen the Covid-19 crisis hugely boost interest in the wave of startups democratizing automation, as companies try to build resilience into their supply chains. If you’re an exec thinking through this kind of thing right now, the way we see it, using Arculus’s technology is just common sense”.

Asked why it is only now that assembly lines can be reinvented, the Atomico VC says a number of building blocks weren’t in place until now. They include cheap, versatile sensors, reliable connectivity, “sufficiently powerful compute resources”, machine vision, and “learning-driven” control systems.

“And even if the tech could have been deployed, the motivation doesn’t come until you buckle under the pressure of increasing product customisation,” he says. “High-speed linear production lines are pretty efficient if you’re only producing one thing, ideally in one colour. But as this has become less and less the case, the industry reacted by incrementally improving, such as adding sub-assemblies that feed into the main line. You can only go so far with that… to be really efficient you’ve got to start fresh and be modular from the ground up. That’s hard”.

Meanwhile, Arculus also counts a number of German entrepreneurs as previous backers. They include Hakan Koc (founder of Auto 1), Johannes Reck (founder of GetYourGuide), Valentin Stalf (founder of N26), as well as the founders of Flixbus.

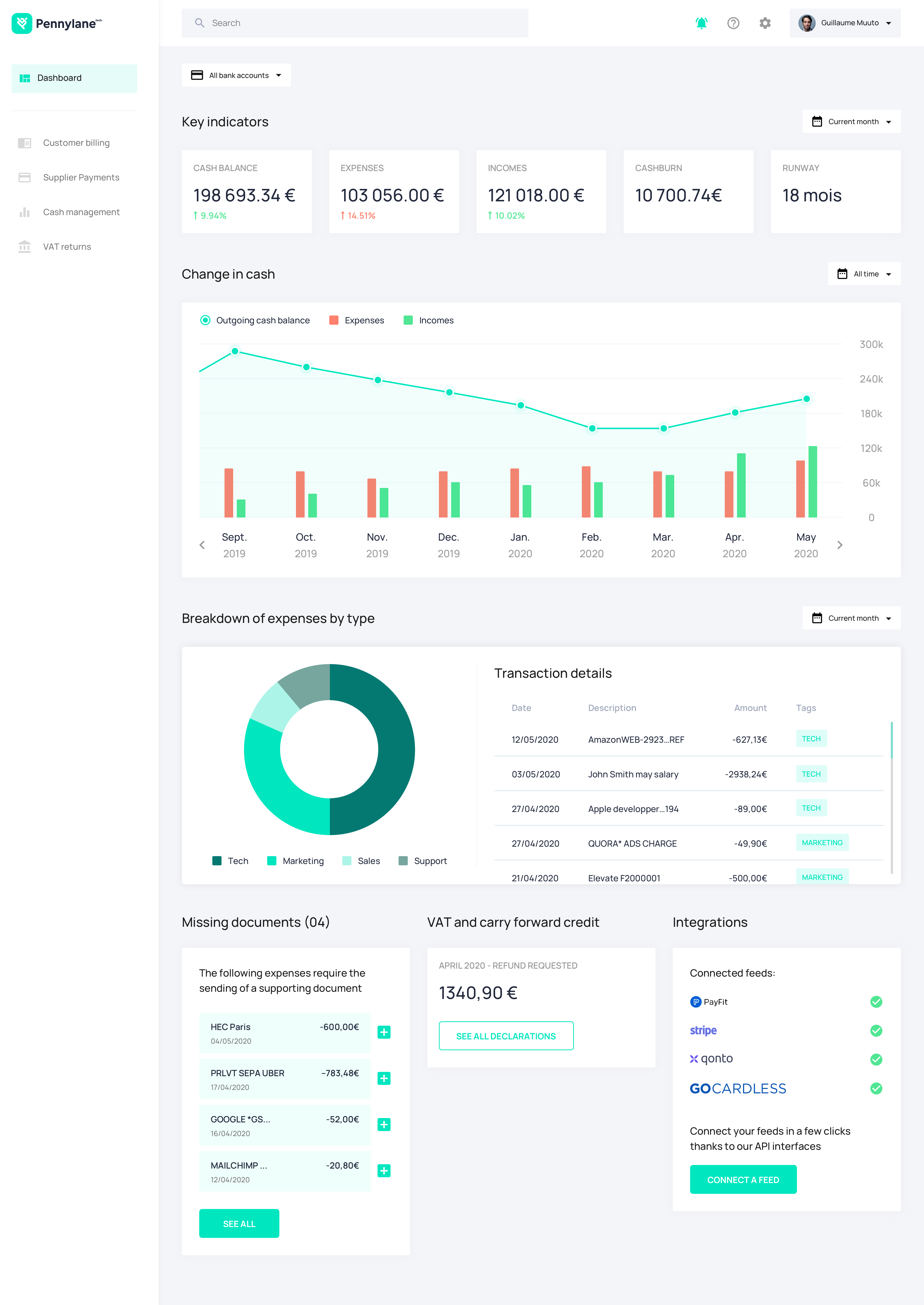

Meet Pennylane, a new French startup that is a building a full-stack service to deal with your financial data. With Pennylane, you get a real-time view of your financial data and you don’t have to work with an accounting company — the startup hires accountants for you.

The startup just raised a $4.3 million (€4 million) seed round with Global Founders Capital, Partech and Kima Ventures. Pennylane’s founders previously worked on PriceMatch, a startup that was acquired by Booking.com in 2015.

“We invested in 25 to 30 startups — we went to see them and asked them what was missing,” Pennylane co-founder Arthur Waller told me. The team realized that there was a big discrepancy between accountants and CEOs.

Many companies work with third-party accounting companies but don’t see the direct benefits of that relationship beyond complying with the law. And yet, accountants have access to all the financial data of the company.

Usually, accountants receive data once a month in a very unstructured way. They waste a ton of time entering data in accounting software. As for companies, a CEO doesn’t know how to use accounting software and can’t take advantage of the accountant’s work to see if there’s any outstanding invoice, if clients haven’t been billed or how your company is doing financially.

That’s why many companies end up using Excel for financial projections and visibility. It’s a big waste of time as you need to connect to multiple services to download invoices, receipts, pay slips and more.

Pennylane aggregates all your financial information using APIs. You set it once and your data is automatically fetched in Pennylane. For instance, you can connect your Pennylane account with your bank account, Stripe, GoCardless, Revolut, PayFit, etc. And if you store your invoices on Google Drive, you can also connect Pennylane with your Google Drive account.

The service then tries to go through this data set on its own as much as much as possible. The company uses optical character recognition and pre-fills accounting information. The result is that companies get a clear overview of their financial data.

“Software alone isn’t going to solve that problem,” Waller said. So Pennylane has hired eight accountants who can check data, correct information if there’s anything wrong and make sure you comply with the law.

By saving time on data entry, accountants can focus on other tasks that they couldn’t handle in the past. “We want to provide a service at the same price as a traditional accounting service but that is ten times better,” Waller said.

The company started accepting customers in March and now has 117 customers, such as Luko, Liberkeys and Pricemoov. Pennylane targets medium companies, those that need to outsource their accounting because it is too complicated but don’t have an in-house accountant.

SoftBank Group Corp. is currently seeking buyers for about $20 billion of its shares in T-Mobile US, according to reports in the Wall Street Journal and Bloomberg. If the proposed sale goes through, its proceeds could help offset SoftBank’s heavy investment losses over the past year.

According to its first-quarter earnings report yesterday, SoftBank’s Vision Fund lost $17.4 billion in value for the year ended March 31, obliterating the $12.8 billion gain the fund recorded a year ago. Earlier this year, the company announced plans to sell up to $41 billion of its assets to increase its share buyback program.

Bloomberg reports that under the proposed deal, which could be announced this week, SoftBank would sell part of its stake to Deutsche Telekom AG, T-Mobile’s parent company. Deutsche Telekom currently owns about 44% of T-Mobile’s shares, but would achieve majority ownership if the deal with SoftBank goes through. Softbank would then sell some of its remaining stake to other investors in a secondary offering.

T-Mobile is the United States’ third-largest wireless carrier, after AT&T and Verizon Wireless*, and it has a current market capitalization of about $126 billion, which means SoftBank’s stake is worth about $31 billion, while Deutsche Telekom’s is about $55 billion.

According to the Wall Street Journal, banks including Morgan Stanley and Goldman Sach Group are currently seeking investors for the proposed sale.

*Disclosure: Verizon is TechCrunch’s parent company.

Confirming the North American job cuts, Pollen co-founder and CEO Callum Negus-Fancey (pictured right) told TechCrunch that 24 team members in Las Vegas have been axed, 29 in LA, 6 in Canada, and 10 that worked remote throughout U.S. That’s a cull of approximately 31% of Pollen’s 216 staff overall.

Confirming the North American job cuts, Pollen co-founder and CEO Callum Negus-Fancey (pictured right) told TechCrunch that 24 team members in Las Vegas have been axed, 29 in LA, 6 in Canada, and 10 that worked remote throughout U.S. That’s a cull of approximately 31% of Pollen’s 216 staff overall.