Before you hire a marketing consultant who doesn’t understand your products or commit to a CMO who has several years of experience — but none in your sector — consider influencer marketing.

If the phrase evokes images of celebrities hawking hard seltzer, think again: An influencer can be as humble as an enthusiastic Reddit user who manages your Telegram channel.

According to Uber growth marketing manager Jonathan Martinez:

“ … You don’t need to find influencers with millions of followers. Instead, lean toward microinfluencers for testing, which will bring cost efficiency and the ability to sponsor a diverse range of people.”

If your startup has a clear brand pitch, “an enticing offer” and “clear next steps,” you’re ready to reach out to influencers, he says.

In a guest post, Martinez explains how to structure offers that will maximize conversions and keep your representatives motivated to promote your products and services.

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Image Credits: Julian Shapiro

This morning, we published an interview with growth expert Julian Shapiro, a founder and angel investor who also advises startups on the best way to present themselves.

Marketing is data-driven, but good storytelling is an art, says Shapiro.

To connect with consumers on an emotional level, “you need a mix of goodwill, what-we-stand-for ideology, social prestige and customer delight — among other affinity-building ingredients.”

Thanks very much for reading Extra Crunch this week!

Walter Thompson

Senior Editor, TechCrunch

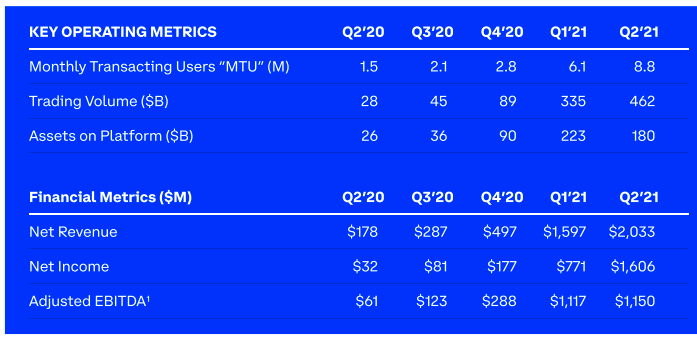

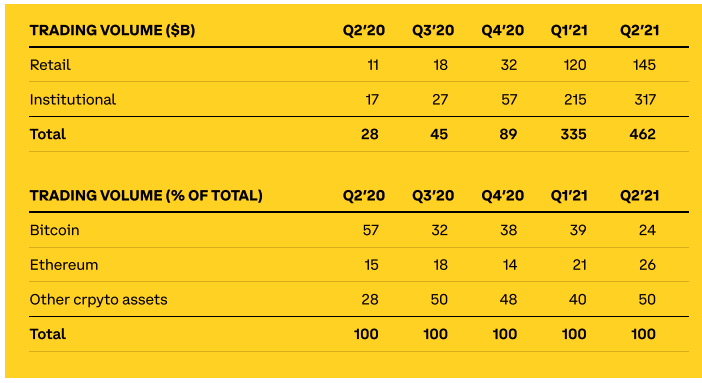

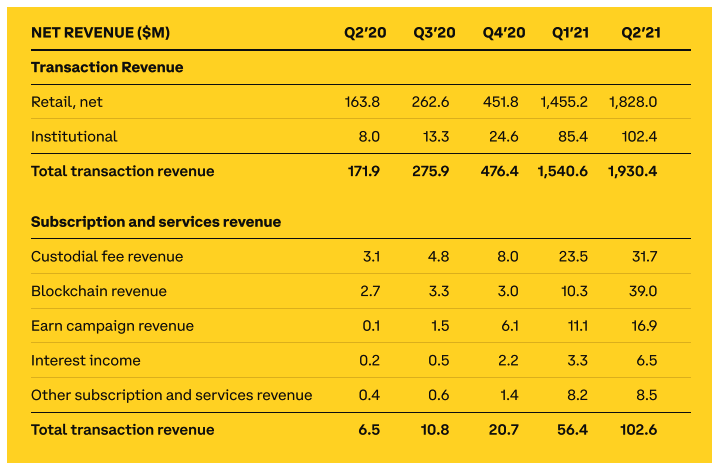

Everyone wants to fund the next Coinbase

Image Credits: Nigel Sussman (opens in a new window)

“In celebration of Coinbase’s earnings report today, investors poured a mountain of cash into one of the company’s global competitors,” Alex Wilhelm writes in The Exchange.

Rolling up his sleeves, he dug into numbers from Coinbase, FalconX and FTX to give readers some perspective on the state of cryptocurrency exchanges.

How to hire and structure a growth team

Image Credits: tomertu (opens in a new window) / Getty Images

Companies that have reached $5 million to $10 million in annual revenue are more likely to assemble growth teams; it’s a smart investment for any startup that’s achieved product-market fit.

It can also be potentially disruptive: Early marketing and product managers may feel sidelined by new cross-functional teams that suddenly take a leadership role.

In a detailed walkthrough, senior director of growth at OpenView Sam Richard explains the core players needed to build a growth team and how to integrate them into the organization smoothly, and shares some useful experiments to run.

“Don’t expect a single hire to scratch the growth itch for you,” Richard warns.

“A brilliant hire is going to come up with ideas, but will absolutely need a team to support them, turn them into experiments and then make them a reality.”

Indiegogo’s CEO on how crowdfunding navigated the pandemic

Image Credits: Bryce Durbin

In an interview with Brian Heater, Indiegogo CEO Andy Yang spoke about how the pandemic has impacted the crowdfunding platform, the challenges of stepping into the role after the previous CEO departed, and how the company reached profitability.

The company wasn’t profitable when you joined?

We weren’t profitable. I joined and then we cut to profitability, or at least kind of a neutral state, and with any kind of change in leadership, some tenured folks opted out, and we basically became a new team overnight to kind of re-found the company, and we’ve been slowly adding people over the last couple years, but always with that eye on profitability and controlling our own destiny.

Kickstarter’s CEO on the future of crowdfunding

Image Credits: Bryce Durbin

Last week, Kickstarter announced that people have backed more than 200,000 projects with $6 billion in pledges since the company launched in 2009. Just 15 months ago, it crossed the $5 billion threshold.

Brian Heater spoke to CEO Aziz Hasan, who took over in 2019, about last year’s substantial of layoffs, the pandemic’s long-term impact on crowdfunding, and how he’s working to build a more resilient company:

I think for us some of the most important things are to really just understand how we’re operating the business, making sure that we are sufficient in the buffer that we have for the business to make sure that we’re operating in a way that we can feel confident that the team is going to have some stability, that they’re going to have this resilience.

Craft your pitch deck around ‘that one thing that can really hook an investor’

We frequently run articles with advice for founders who are working on pitch decks. It’s a fundamental step in every startup’s journey, and there are myriad ways to approach the task.

Michelle Davey of telehealth staffing and services company Wheel and Jordan Nof of Tusk Venture Partners appeared on Extra Crunch Live recently to analyze Wheel’s Series A pitch.

Nof said entrepreneurs should candidly explain to potential investors what they’ll need to believe to back their startup.

” … It takes a lot of guesswork out of the equation for the investor and it reorients them to focus on the right problem set that you’re solving,” he said.

“You get this one shot to kind of influence what they think they need to believe to get an investment here … if you don’t do that … we could get pretty off base.”

Online retailers: Stop trying to beat Amazon

Image Credits: TravelCouples (opens in a new window) / Getty Images

Going up against global e-commerce behemoth Amazon might seem futile, but smaller players can leverage value adds that give them a leg up when it comes to ensuring a loyal customer base, says Kenny Small, vice president SAP and Enterprise at Qualitest Group.

“The reality is that Amazon’s true unique selling proposition is its distribution network,” he writes in a guest post. “Online retailers will not be able to compete on this point because Amazon’s distribution network is so fast.

“Instead, it’s important to focus on areas where they can excel — without having to become a third-party seller on Amazon’s platform.”

The China tech crackdown continues

Image Credits: Nigel Sussman (opens in a new window)

Edtech and fintech have been in the Chinese Communist Party crosshairs in recent weeks — now, chat apps and gaming are among the targets.

Beijing filed a civil suit against Tencent over claims that its WeChat Youth Mode flouts laws protecting minors, and state media criticized the gaming industry as the digital equivalent of passing out drugs to kids, Alex Wilhelm writes in The Exchange.

He writes that the “news appears to indicate that we should expect more of the same as we’ve seen in recent months from the Chinese government: More complaints about the impact of ‘excessive’ capital in its industries, more tumbling share prices and more held IPOs.”

5 ways AI can help mitigate the global shipping crisis

Image Credits: Yuichiro Chino (opens in a new window) / Getty Images

In an increasingly on-demand world, shipping delays and disruptions are a major roadblock to customer happiness.

AI can help, says Ahmer Inam, chief artificial intelligence officer at Pactera EDGE, who offers five strategies for using AI that can help startups understand supply chain disruptions and prepare for a Plan B.

“While AI won’t protect startups, manufacturers and retailers from these types of disruptions in the future, it can help them sense, anticipate, reroute and respond to them more effectively.”