YouTube earlier this year announced its plans to significantly invest in original creator content for its TikTok competitor, YouTube Shorts, with the introduction of a $100 million YouTube Shorts Fund. The fund will reward creators for their most engaging and most viewed short-form videos over the course of 2021 to 2022, with the goal of quickly scaling creator activity on YouTube’s new short-form video platform, Shorts, to better rival TikTok. Today, YouTube announced the fund is officially launching and creators will begin to receive their first payouts in August.

Image Credits: YouTube

Every month, YouTube will invite thousands of eligible creators to claim a payment from the fund. These payouts may range anywhere from $100 to $10,000, based on viewership and engagement with their Shorts videos. Reached for comment, YouTube declined to share the exact viewership thresholds creators will have to reach to earn the payouts, saying that those numbers may change from month to month.

The company told TechCrunch it will determine how it calculates the thresholds by analyzing the best-performing channels and then calculating their bonus based on a number of factors, which includes views, where their audience is located and more. The company also said it wanted to make sure it was rewarding as many creators as possible, which is why it set a minimum payment of $100.

To qualify, creators must produce original content — not videos that were re-uploaded from other channels or those with watermarks from other social services. That was a problem that Instagram’s TikTok competitor Reels has faced — creators often re-used the same content they’re sharing on TikTok when they publish to Reels. To fight the problem, Instagram even had to adjust its algorithm to downrank the recycled content.

While there are plenty of tools that allow creators to strip the watermark from a video, as well as those that let you edit videos for upload to multiple short-form video platforms, YouTube says it will be using a combination of automation and human reviewers to ensure creators meet its guidelines around original content.

Creators will also need to be 13 or older in the U.S., or the age of majority in other countries and regions, to quality. Those ages 13 to 18 will also need to have a parent or guardian set up their AdSense account, link it to the creator’s channel and accept the terms, as this is where payments will be directed. All of a creator’s Shorts videos will count toward their bonuses each month they receive views — not just the month they were uploaded, YouTube notes.

The channels also need to have uploaded at least one eligible Short in the last 180 days and must follow YouTube’s Community Guidelines, copyright rules and monetization policies. While YouTube Partner Program members can participate in the fund, creators don’t have to already be monetizing on YouTube to quality for the new Shorts bonuses.

At launch, the fund will support creators in the U.S., Brazil, India, Indonesia, Japan, Mexico, Nigeria, Russia, South Africa and the United Kingdom. Over time, it will expand to more markets.

Image Credits: YouTube

The company also told us it’s not looking for any specific types of video to reward, as the fund gets off the ground. Instead, it’s only looking at the metrics, like the total monthly performance a channel’s Shorts received.

On the one hand, not specifying any video categories or subject matter to lean into gives creators a lot of freedom to experiment when producing Shorts. But on the other, it could also lead creators to simply make more TikTok-like content, but publish it to YouTube instead in hopes of cashing in. That could result in YouTube Shorts feeling a lot like the TikTok clone that it is, rather than allowing it to differentiate itself by the nature of its content.

For comparison, other TikTok rivals, like Pinterest’s Idea Pins or Snapchat’s Spotlight aim to leverage what makes their platform unique and deliver that as short-form, public videos. Pinterest’s Idea Pins are often focused on tutorials or recipe-making, which are popular searches on its service. Spotlight, meanwhile, can feature Snaps — including those from private accounts, not professionals. That makes some Spotlight videos feel less polished and produced, compared with TikTok or Reels, which fits in with its more casual aesthetic.

YouTube says it will begin reaching out to creators starting next week to let them know if they’ve qualified for a bonus. The company will send a notification in the YouTube app, which includes the amount of the bonus and details on how to claim it. Creators will then have until the 25th of the month to claim the bonus payment before it expires.

Image Credits: YouTube

TikTok’s growth and popularity has encouraged a number of social platforms to invest directly in the creator community in hopes of winning back some of their audience. Facebook recently announced its own $1 billion-plus bonus system for videos across both Facebook and Instagram through the end of 2022, including but not limited to Reels videos. Snap initially said it would distribute $1 million per day through the end of 2020 for top Snaps on Spotlight, but later dialed that back. Pinterest announced a much smaller ($500,000) creator fund that runs through 2021.

And to counteract all the challenges, TikTok last month introduced a $200 million fund for U.S. creators.

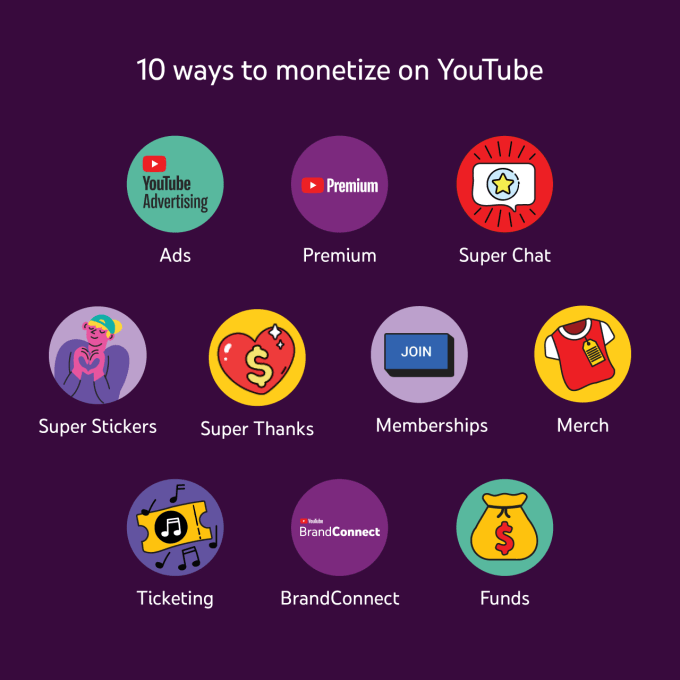

With the official launch of the Shorts Fund, YouTube notes it now has 10 ways creators can make money on its platform, including ads, YouTube Premium subscription revenue shares, channel memberships, Super Chat, Super Thanks, Super Stickers, merchandise, ticketing and YouTube BrandConnect.