Priscilla Chan is so much more than Mark Zuckerberg’s wife. A teacher, doctor, and now one of the world’s top philanthropists, she’s a dexterous empath determined to help. We’ve all heard Facebook’s dorm-room origin story, but Chan’s epiphany of impact came on a playground.

In this touching interview this week at TechCrunch Disrupt SF, Chan reveals how a child too embarrassed to go to class because of their broken front teeth inspired her to tackle healthcare. “How could I have prevented it? Who hurt her? And has she gotten healthcare, has she gotten the right dental care to prevent infection and treat pain? That moment compelled me, like, ‘I need more skills to fight these problems.'”

That’s led to a $3 billion pledge towards curing all disease from the Chan Zuckerberg Initiative’s $45 billion-plus charitable foundation. Constantly expressing gratitude for being lifted out of the struggle of her refugee parents, she says “I knew there were so many more deserving children and I got lucky”.

Here, Chan shares her vision for cause-based philanthropy designed to bring equity of opportunity to the underserved, especially in Facebook’s backyard in The Bay. She defends CZI’s apolitical approach, making allies across the aisle despite the looming spectre of the Oval Office.And she reveals how she handles digital well-being and distinguishes between good and bad screen time for her young daughters Max and August. Rather than fielding questions about Mark, this was Priscilla’s time to open up about her own motivations.

Most importantly, Chan calls on us all to contribute in whatever way feels authentic. Not everyone can sign the Giving Pledge or dedicate their full-time work to worthy causes. But it’s time for tech’s rank-and-file rich to dig a little deeper. Sometimes that means applying their engineering and product skills to develop sustainable answers to big problems. Sometimes that means challenging the power structures that led to the concentration of wealth in their own hands. She concludes, “You can only try to break the rules so many times before you realize the whole system’s broken.”

Token structuring and tokeneconomics are among of the most important considerations when designing a blockchain. When thinking about how best to distribute these tokens, founders often think about how the tokens will impact external stakeholders such as their investors, the community, and stakers (people that can mine or validate block transactions according to how many coins he or she holds). But token economies are also bringing disruption to organizations internally, especially when it comes to HR and compensation.

If the tokens are structured properly for a blockchain, external stakeholders will be directly aligned with the goal of the project. Those incentives can encourage participation on the blockchain platform and/or drive token demand with community-building and marketing. Similarly, if internal stakeholder incentives are structured correctly, the project could accrue long-term value by motivating employees to work towards the same goal, while reducing adversarial behavior and also bad actors.

For any blockchain company to succeed long-term and scale, it’s inevitable that they need to structure their tokens to retain and reward the best employees sustainably. This is as important it not more important than incentivizing external token holders.

How does an employee look at tokens vs equity?

Currently, equity in the form of stock options is widely distributed as part of compensation packages amongst startups. When employees join a company, they are usually offered a combination of cash and stock options. The options become a way for the employees to meaningfully participate in a company’s upside should they succeed. Often, employees can negotiate between taking a higher cash comp or higher options amount, depending on their risk appetite.

There are many ways tokens and equity are similar. For one, both assets motivate individuals to align their goals with that of a company’s. If the company becomes more successful, the value of its tokens and equity should theoretically go up. Nonetheless, one of the downsides of stock options is that they usually require a liquidity event for an employee to convert them to paper money. Historically, that was when a company went public and the employee could convert their options into stocks and then sell them in the public markets.

However, in the last decade, with the increasing amount of private capital and subsequent larger private fundraising rounds, companies are taking way longer to IPO. Companies such as Dropbox took eleven years from founding to IPO, while Airbnb has been around ten years and still hasn’t gone public. As a result, private companies started doing option buybacks to provide liquidity for their employees. Simultaneously, this phenomenon has caused the secondary market to thrive in Silicon Valley.

Token liquidity changes the game

One of the largest differences between tokens and equity is that tokens are immediately liquid, assuming that they have already been listed on an exchange. To put simply, equity options only prove their value at the end, whereas tokens have certainty values from the beginning.

Now in cryptocurrency and blockchain companies, employees could get paid in tokens in lieu of equity or cash, primarily outside of the U.S. Many tokens have a liquidity advantage over equity. For example, it can be immediately sold upon reception, assuming that the token has been listed on an exchange and there is enough trading volume.

This is also one of the reasons why exchanges are so important for the cryptocurrency space because 1) it’s one of the easier ways to gauge the value of a company given that the industry has yet to figure out a proper valuation methodology, and 2) it provides immediate liquidity for employees who have been burned by the hopes a billion dollar company not coming to fruition and all the options going to zero.

For an employee looking for a job in a technology-based company, consider two companies that are exactly the same, with the same team quality and same targeted industry, but one company has a token incentive structure instead of an equity incentive structure, and the token is already traded on an exchange. Why would the employee ever want equity? With tokens, you’d still share the upside in the company’s success, but also have immediate liquidity.

Additionally, outside the U.S., often employees can also get paid in tokens or stable coins in lieu of cash to take advantage of tax benefits given the lack of regulatory sophistication. That may change very soon, however. Token structure, therefore, is a disruption to a company’s internal structure and we will share some examples below of how that’s already affecting a number of Chinese crypto companies.

Token incentives will disrupt traditional ways of compensating employees

These changes to employee compensation have already become popular in places like China, where a number of Chinese blockchain companies have started on the foundation of distributing tokens as compensation. Companies like Ontology, NEO, Huobi, and Binance pay their employees in their own tokens. Many of these teams operate worldwide but they are able to manage hundreds of people, often with just a handful of HR staff, through a shared incentive structure.

In the case of Neo, the original founding team, in fact, didn’t have anyone with a computer science background. When they were looking for developers, they would pay tokens to people to do development work for them. For Ontology, it was even more extreme. The founding team initially set up the Ontology Foundation. They didn’t want to hire people, so instead, they listed out a list of things that needed to be developed and paid tokens to all the developers who contributed.

Binance, similarly, paid their employees in tokens. They would then use their quarterly profits to burn tokens, which subsequently boosted the value of the remaining tokens. It is possible that partially due to these effective token incentives, Ontology has been the best performing token this year while Binance continues to hold the lead in the exchange space.

China has taken a lead here compared to the U.S. partially because of regulatory uncertainties, but there are examples in America as well of these changing compensation norms. In the early days of cryptocurrency when it was (even more) wild west, Consensys got started by compensating their employees in tokens until their first legal hire came along. That story is similar to Coinbase, where initially a number of first employees were given the choice of being paid in coins and/or cash.

Token compensation also seems to be particularly powerful incentives for Chinese blockchain companies, more so than their U.S. counterparts. Maomao Hu, Partner at Eigen Capital and CTO of Calculus Network, talks about the psyche of the young generation of Chinese developers: “Being Chinese, Chinese engineers, especially the young ones, have a hunger that you only see in some parts of Silicon Valley, and that’s like everyone. They are just doing 80 hours 100 hour weeks because they hate being poor and they hate not having an opportunity and they don’t have other ways to get an opportunity, and that’s like everyone.”

It may also be that because there have been fewer technology cycles in China, and the rise of the largest technology companies happened only in the last decade, equity compensation remains a relatively new concept to local citizens. With token compensation introduced, this is the first time for many Chinese people to be able to participate in a company’s upside so directly.

Despite their growing popularity, these incentive schemes are still early and experimental, and there are unforeseen risks associated with token issuance as compensation. In particular, the appeal of short-term, quick gains from tokens is ever more attractive. If wrongly incentivized, people could end up spending time hyping up their tokens instead of building product, allowing employees to cash out quickly without producing.

As a result, serious founders of new token-based companies should be aware of such short-sightedness when designing employee token incentives. They can potentially introduce long-term token vesting schedules, and also hire people who care about driving long-term value. For CEOs, this is going to be an increasingly important role they will have to take in the token economy. I’m certain though that the next set of large unicorns will be coming from tech companies with great token incentives structures, in or outside of the U.S.

For all of the excitement centered around fintech over the past half-decade, most venture-backed fintech companies struggle to acclimate to public markets. LendingClub and OnDeck have plummeted since their late 2014 IPOs after several years of darling status in the private markets. GreenSky, which went public in May of this year, has been unable to return to its IPO price. Square is the exception to the rule.

Sometimes we overlook the companies that hail from the era that precedes the current wave of fintech fascination, a vertical which has accumulated over $100 billion in global investment capital since 2010.

One of these companies is LendingTree, which got its start height of the Internet bubble, going public in mid-February of 2000, less than a month before the Dot-com bubble peaked.LendingTree began in 1996 in a founding story that epitomizes the early Internet era. Doug Lebda, an accountant searching for homes in Pittsburgh, had to manually compare mortgage offers from each bank. So he created a marketplace for loans in the same way OpenTable helps you find your restaurant of choice or Zillow simplifies the home buying process. In the words of Rich Barton, iconic founder of Expedia, Zillow, and Glassdoor, this business is a classic “power to the people play.”

The marketplace business model has been the darling that has driven returns for many of the leading VCs like Benchmark, a16z, and Greylock. Network effects are a non-negotiable part of the explanation as to why. Classic success stories that have transitioned nicely into public markets include Zillow, OpenTable (acq.), Etsy, Booking.com, and Grubhub. LendingTree is often left off of this list, yet, the business sits in a compelling space as consumers and lenders continue to manage their financial lives online.

Insight in a Sea of Ambiguity

The lending process has been defined by significant information asymmetry between borrowers and lenders. Lenders have a disproportionate amount of leverage in the relationship. And that’s not to say it should be different – it’s perfectly logical to require a borrower to prove their creditworthiness. However, aggregation, synthesis, and recommendations modernize a dated dynamic.

Ironically, in an age where consumers are inundated with information,less than 50% of interested borrower’s shop for loans. Most consumers take the first offer they receive. The benefit of a marketplace, however, is price competition and transparency. The ability to shop the market and access the same information that lenders have is a luxury that didn’t exist twenty years ago. The borrowers who do shop through LendingTree reap significant benefits; on average,roughly $14,000 on mortgages and 570 basis points on personal loans. There’s certainly something to be said for comfortability and hand-holding, but at some point the metrics speak for themselves.

LendingTree isn’t a marketplace in the purest sense because of the process that takes place after a borrower clicks “apply.” While a diner can reserve a table at any listed restaurant with OpenTable for dinner tomorrow tonight, she can’t simply take the loan she wants. LendingTree lacks the direct feedback loop between consumers and lenders that characterizes most marketplaces. Instead, the platform aggregates information from a network of over 500 lenders to provide options according consumer’s needs. LendingTree is effectively the onramp for interested borrowers, which necessitates the entry of lenders to fill the borrower’s needs.

As this “onramp” continues to serve a larger audience as more consumers conduct their finances online, banks and lenders intend to seize the opportunity. Digital ad spend in the financial services industry is going to continue to grow rapidly at an estimated 20% CAGR between 2014 and 2020, effectively tripling the size of LendingTree’s core market.

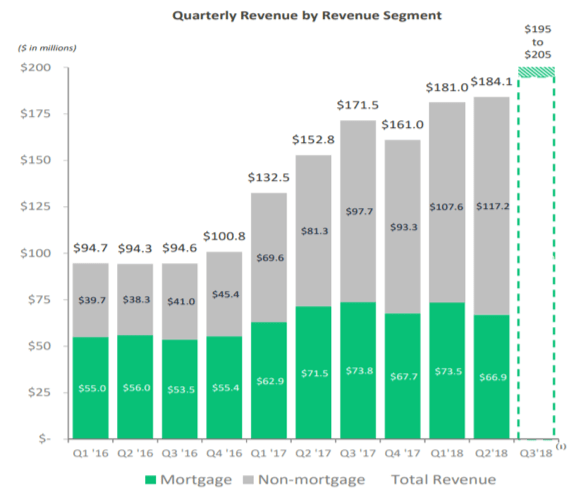

Diversifying away from Mortgages

LendingTree’s revenue mix has change over the years.

For all intents and purposes, LendingTree has been in the mortgage business since its inception. The company experimented with a myriad of business models, including a foray into loan origination through their LendingTree Loans product line, which they ultimately sold off to Discover in 2011. Even in 2013, only 11% of their revenue originated from non-mortgage products.

LendingTree has expanded their platform in a few short years to build their non-mortgage products including credit cards, HELOCs, personal, auto, and small business loans. They have also pursued credit repair services and deposit accounts, with insurance in the pipeline. Whereas mortgage revenue made up roughly 60% of total sales in Q2 2016, it dropped to 36% as of this quarter. They wanted to diversify their product mix, but they realized they were also leaving money on the table.

Through strategic M&A activity, LendingTree has acquired a number of leading media and comparison properties to expand into new products. Acquiring CompareCards, a leading online source for credit card comparisons, has allowed them to catch up to Credit Karma and Bankrate, who own a large part of the existing market. Additional acquisitions in tertiary products like student loans, deposit accounts, and credit services have enabled the company to expand their market share in markets that are both ripe for growth and sparse of competition. The inorganic growth strategy emulates that of two of LendingTree’s major shareholders: Barry Diller, who’s company IAC previously owned LendingTree before spinning them off in 2008, and John Malone, who owned 27% of shares as of November, 2017.

LendingTree has made significant acquisitions to expand and grow

Enhancing Customer Engagement

The potential scale and success of LendingTree’s business model is predicated on discovering prospective borrowers. If they’re repeat customers, that’s a big win because their promotional costs drop significantly once a customer is familiar with the platform.

My LendingTree, the company’s personal financial management (PFM) app launched in 2014, has 8.8 million customers and generates roughly 20% of the company’s leads. It offers free credit scores, credit monitoring, and goals-based guidance through a proprietary credit and debt analyzer. At the surface, it’s not especially different from any of the other leading consumer PFM apps. That’s been the issue with these apps: the service is valuable, but it’s very difficult to differentiate beyond UI/UX, which is far from a defensible moat.

However, the ability for LendingTree to lock in customers and accumulate customer data to personalize product recommendations is a breakthrough for both consumers and lenders. Consumers outsource the loan diligence process to their phone, which explores the universe of lending options in order to find the most suitable options.

LendingTree’s new personal finance management app. (Photo by LendingTree)

The leader in this space is Credit Karma, and by a wide margin. They’re estimated to have around 80 million customers. Those numbers appear starkly different at first glance, but it’s important to keep in mind LendingTree is relatively new, launching in 2014. Credit Karma developed a more captive relationship with customers from their inception in 2007, beginning as a free credit score platform. They’re effectively in an arms race, trying to emulate each other’s primary value propositions in order to win over a larger share of customer attention.

By all accounts, the My LendingTree product is still in its infancy. Personal loans make up nearly two-thirds of revenue generated through My LendingTree. Credit cards were integrated through CompareCards earlier this year; deposits will be integrated in the fourth quarter through DepositAccounts. As the platform more formally integrates mortgage refinancing and HELOCs, there are more channels to drive user engagement.

For the consumer, this app reinforces the aggregation and connection between interested borrowers and willing lenders. Arguably more significant, however, is the personalization of individual customer experience that will drive further engagement and improve the recommendation engine. With the continued migration to online and mobile for financial services, this product benefits from natural demographic tailwinds.

If LendingTree can successfully reengage with customers on a more recurring basis via My LendingTree, the app should be accretive to overall variable marketing margin because they’ll have to spend far less on promotional activities due to organic customer. The combination of a market-leading aggregator with a comprehensive PFM tool creates a flywheel effect where success begets success, particularly with a major head start in the lending aggregation business.

Removing the Informational Asymmetry

In LendingTree’s business model, customer demand drives the flow of ad dollars and ultimately origination volume. Lenders follow customer demand. LendingTree helps expedite that process. Lenders can expand their conversions by boosting the number of high-quality leads and reducing obstacles to the loan application process. LendingTree improves both catalysts.

On the lender side, My LendingTree fundamentally changes LendingTree’s value proposition. They used to be responsible for connecting lenders with warm leads to drive conversions. With an existing customer base, the lead generation suddenly gets easier. It also significantly reduces the customer acquisition cost for lenders, notoriously a major component of their expense profile.

Nearly 50% of all consumer interactions with banks and financial services companies occur online. It’s not controversial to say that figure is likely heading in only one direction. Currently, credit cards and personal loans are the most automated online application processes because the decisioning occurs relatively quickly. Of the expansive network of mortgage lenders on LendingTree’s platform, only 40 currently enable borrowers to continue their application online. As mortgages and small business loans become more automated through partnerships with third-parties like Blend and Roostify, LendingTree will benefit from more seamless integrations and likely, higher conversions.

The real value proposition for the lender, however, is in the headcount consolidation. Just as the number of stock brokers and equity traders has diminished significant, the role of the loan officer will follow a similar trajectory. LendingTree initially supplemented loan officers in their borrower sourcing from a marketing perspective, which drove loan officer commissions down significantly.

Doug Lebda’s next conquest is to supplant the entire sales function. In response to a question about LendingTree’s impact on lender headcount, Lebda responded: “what will happen is [lenders will] be able to reduce commission. So the real competitor, if you will, to LendingTree…is the fully commissioned loan officer…In the future, you’re going to have LendingTree convincing the borrower through technology and then you’re going to have an individual lender just basically processing and getting it through.”

The relationship between a loan officer and a prospective borrower is marred by informational asymmetry. Incentives aren’t aligned.Soon enough, the pre-approval process launched through their new digital mortgage experience, “Rulo” will help to solve a problem that has plagued LendingTree since its inception: an exhaustive pursuit from loan officers.

With Rulo, LendingTree sorts and filters the list of offers and provides a recommendation based on the best option. Then, the app allows you to contact the lender directly, offering the consumer the freedom they historically haven’t had. Commenting on the early success of the new experience, Lebda said “[the conversion rate is] literally about triple what it is on the LendingTree experience.” LendingTree is streamlining a low value, yet operationally costly element of the lending business that has remained more or less stagnant for half a century.

Seeing the Forrest through the Trees

The fawning over fintech companies has driven exorbitant amounts of global investment from venture capitalists and private equity firms who are ultimately looking for exit opportunities. Two things are happening: first, most of the major fintech companies aren’t going public, although that is beginning to change. Second, and perhaps more importantly, the ones that do go public don’t fare particularly well.

The tried and true strategy of most emerging financial technology startups is to focus on user growth and monetize later. LendingTree did the opposite; they created a cash-flow generating platform that served a critical purpose, simplifying a historically complex landscape for consumers, while simultaneously driving directly attributable revenue for lenders. They have proved their original value proposition, connecting borrowers with lenders, and now they’re playing catch up to provide supplementary tools to add more value for customers. It’s a rare pathway, but a productive one that more fintech startups should consider.

“Unmortgage enables everyone to live in the home they want to, that’s our mission,” Unmortgage co-founder and CEO Ray Rafiq-Omar tells me. “We do that by allowing people to buy as little as five percent of a home and rent the rest. So there’s no mortgage involved, hence the name Unmortgage”.

The burgeoning London startup, which aims to launch next year having just closed a hefty £10 million seed round, calls its model “part-own, part-rent”. However, unlike traditional shared ownership schemes, Unmortgage doesn’t want you to have to take out a mortgage to buy the first portion of your own, and it isn’t targeting new-builds.

Like a number of other fintech/proptech companies, such as Strideup and Proportunity, it is the latest attempt to solve the increasing difficulty first time buyers face trying to get on the housing ladder as rising house prices typically outstrip wages. If people rent, they often cannot save the large deposit required for a mortgage. It is this “vicious circle” that Unmortgage want to break: by helping families that can afford to rent gradually buy a home.

“The way we like to think about it is the security of home ownership with the flexibility of renting,” says Rafiq-Omar. “You find a home. If we like it too, we’ll but it together in partnership. You’ll own your bit and you’ll pay rent on our bit. Then you have the option to buy more of your home from as little as a pound at any time”.

To keeps things fair — Rafiq-Omar stresses that fairness is “our core value” — Unmortgage will revalue the property on a monthly basis so you’ll always have an up-to-date valuation when increasing your stake. And at any point you are free to either buy out Unmortgage with a mortgage or an inheritance or to give the company three month’s notice for it to buy you out so you can take your cash at market price and move on to your next home.

Likewise, the rent you pay on the part of the property you don’t own is pegged to rises to inflation. But in case inflation outpaces market rate rents, Rafiq-Omar says Unmortgage will allow the customer to ask for a rent review. “They have the ability to not have to worry about their rent but if they are worried they can have it reviewed,” he says.

Unmortgage will use institutional funding to finance its part of the homes it purchases, who Rafiq-Omar says would like to own residential property, and the secure income stream it brings, but don’t want to be landlords or end up in the media for behaving like a landlord. “Unmortgage gives them a way to invest in residential property while solving societal need, which is [that] people want to own their own homes and have security over their housing situation”.

Meanwhile, investors in Unmortgage’s seed round are fintech venture capital firms Anthemis Exponential Ventures, and Augmentum Fintech plc. “”We’re grateful to our investors for believing in us and our social mission and excited to be working with them – especially Tee Pruitt [of Anthemis], who was instrumental through much of this process,” adds Rafiq-Omar.

Half an hour into their two-hour testimony on Wednesday before the Senate Intelligence Committee, Facebook COO Sheryl Sandberg and Twitter CEO Jack Dorsey were asked about collaboration between social media companies. “Our collaboration has greatly increased,” Sandberg stated before turning to Dorsey and adding that Facebook has “always shared information with other companies.” Dorsey nodded in response, and noted for his part that he’s very open to establishing “a regular cadence with our industry peers.”

Social media companies have established extensive policies on what constitutes “hate speech” on their platforms. But discrepancies between these policies open the possibility for propagators of hate to game the platforms and still get their vitriol out to a large audience. Collaboration of the kind Sandberg and Dorsey discussed can lead to a more consistent approach to hate speech that will prevent the gaming of platforms’ policies.

But collaboration between competitors as dominant as Facebook and Twitter are in social media poses an important question: would antitrust or other laws make their coordination illegal?

The short answer is no. Facebook and Twitter are private companies that get to decide what user content stays and what gets deleted off of their platforms. When users sign up for these free services, they agree to abide by their terms. Neither company is under a First Amendment obligation to keep speech up. Nor can it be said that collaboration on platform safety policies amounts to collusion.

This could change based on an investigation into speech policing on social media platforms being considered by the Justice Department. But it’s extremely unlikely that Congress would end up regulating what platforms delete or keep online – not least because it may violate the First Amendment rights of the platforms themselves.

What is hate speech anyway?

Trying to find a universal definition for hate speech would be a fool’s errand, but in the context of private companies hosting user generated content, hate speech for social platforms is what they say is hate speech.

Facebook’s 26-page Community Standards include a whole section on how Facebook defines hate speech. For Facebook, hate speech is “anything that directly attacks people based on . . . their ‘protected characteristics’ — race, ethnicity, national origin, religious affiliation, sexual orientation, sex, gender, gender identity, or serious disability or disease.” While that might be vague, Facebook then goes on to give specific examples of what would and wouldn’t amount to hate speech, all while making clear that there are cases – depending on the context – where speech will still be tolerated if, for example, it’s intended to raise awareness.

Twitter uses a “hateful conduct” prohibition which they define as promoting “violence against or directly attacking or threatening other people on the basis of race, ethnicity, national origin, sexual orientation, gender, gender identity, religious affiliation, age, disability, or serious disease.” They also prohibit hateful imagery and display names, meaning it’s not just what you tweet but what you also display on your profile page that can count against you.

Both companies constantly reiterate and supplement their definitions, as new test cases arise and as words take on new meaning. For example, the two common slang words to describe Ukrainians by Russians and Russians by Ukrainians was determined to be hate speech after war erupted in Eastern Ukraine in 2014. An internal review by Facebook found that what used to be common slang had turned into derogatory, hateful language.

Would collaboration on hate speech amount to anticompetitive collusion?

Under U.S. antitrust laws, companies cannot collude to make anticompetitive agreements or try to monopolize a market. A company which becomes a monopoly by having a superior product in the marketplace doesn’t violate antitrust laws. What does violate the law is dominant companies making an agreement – usually in secret – to deceive or mislead competitors or consumers. Examples include price fixing, restricting new market entrants, or misrepresenting the independence of the relationship between competitors.

A Pew survey found that 68% of Americans use Facebook. According to Facebook’s own records, the platform had a whopping 1.47 billion daily active users on average for the month of June and 2.23 billion monthly active users as of the end of June – with over 200 million in the US alone. While Twitter doesn’t disclose its number of daily users, it does publish the number of monthly active users which stood at 330 million at last count, 69 million of which are in the U.S.

There can be no question that Facebook and Twitter are overwhelmingly dominant in the social media market. That kind of dominance has led to calls for breaking up these giants under antitrust laws.

Would those calls hold more credence if the two social giants began coordinating their policies on hate speech?

The answer is probably not, but it does depend on exactly how they coordinated. Social media companies like Facebook, Twitter, and Snapchat have grown large internal product policy teams that decide the rules for using their platforms, including on hate speech. If these teams were to get together behind closed doors and coordinate policies and enforcement in a way that would preclude smaller competitors from being able to enter the market, then antitrust regulators may get involved.

Antitrust would also come into play if, for example, Facebook and Twitter got together and decided to charge twice as much for advertising that includes hate speech (an obviously absurd scenario) – in other words, using their market power to affect pricing of certain types of speech that advertisers use.

In fact, coordination around hate speech may reduce anti-competitive concerns. Given the high user engagement around hate speech, banning it could lead to reduced profits for the two companies and provide an opening to upstart competitors.

Sandberg and Dorsey’s testimony Wednesday didn’t point to executives hell-bent on keeping competition out through collaboration. Rather, their potential collaboration is probably better seen as an industry deciding on “best practices,” a common occurrence in other industries including those with dominant market players.

What about the First Amendment?

Private companies are not subject to the First Amendment. The Constitution applies to the government, not to corporations. A private company, no matter its size, can ignore your right to free speech.

That’s why Facebook and Twitter already can and do delete posts that contravene their policies. Calling for the extermination of all immigrants, referring to Africans as coming from shithole countries, and even anti-gay protests at military funerals may be protected in public spaces, but social media companies get to decide whether they’ll allow any of that on their platforms. As Harvard Law School’s Noah Feldman has stated, “There’s no right to free speech on Twitter. The only rule is that Twitter Inc. gets to decide who speaks and listens–which is its right under the First Amendment.”

Instead, when it comes to social media and the First Amendment, courts have been more focused on not allowing the government to keep citizens off of social media. Just last year, the U.S. Supreme Court struck down a North Carolina law that made it a crime for a registered sex offender to access social media if children use that platform. During the hearing, judges asked the government probing questions about the rights of citizens to free speech on social media from Facebook, to Snapchat, to Twitter and even LinkedIn.

Justice Ruth Bader Ginsburg made clear during the hearing that restricting access to social media would mean “being cut off from a very large part of the marketplace of ideas [a]nd [that] the First Amendment includes not only the right to speak, but the right to receive information.”

The Court ended up deciding that the law violated the fundamental First Amendment principle that “all persons have access to places where they can speak and listen,” noting that social media has become one of the most important forums for expression of our day.

Lower courts have also ruled that public officials who block users off their profiles are violating the First Amendment rights of those users. Judge Naomi Reice Buchwald, of the Southern District of New York, decided in May that Trump’s Twitter feed is a public forum. As a result, she ruled that when Trump blocks citizens from viewing and replying to his posts, he violates their First Amendment rights.

The First Amendment doesn’t mean Facebook and Twitter are under any obligation to keep up whatever you post, but it does mean that the government can’t just ban you from accessing your Facebook or Twitter accounts – and probably can’t block you off of their own public accounts either.

Collaboration is Coming?

Sandberg made clear in her testimony on Wednesday that collaboration is already happening when it comes to keeping bad actors off of platforms. “We [already] get tips from each other. The faster we collaborate, the faster we share these tips with each other, the stronger our collective defenses will be.”

Dorsey for his part stressed that keeping bad actors off of social media “is not something we want to compete on.” Twitter is here “to contribute to a healthy public square, not compete to have the only one, we know that’s the only way our business thrives and helps us all defend against these new threats.”

He even went further. When it comes to the drafting of their policies, beyond collaborating with Facebook, he said he would be open to a public consultation. “We have real openness to this. . . . We have an opportunity to create more transparency with an eye to more accountability but also a more open way of working – a way of working for instance that allows for a review period by the public about how we think about our policies.”

I’ve already argued why tech firms should collaborate on hate speech policies, the question that remains is if that would be legal. The First Amendment does not apply to social media companies. Antitrust laws don’t seem to stand in their way either. And based on how Senator Burr, Chairman of the Senate Select Committee on Intelligence, chose to close the hearing, government seems supportive of social media companies collaborating. Addressing Sandberg and Dorsey, he said, “I would ask both of you. If there are any rules, such as any antitrust, FTC, regulations or guidelines that are obstacles to collaboration between you, I hope you’ll submit for the record where those obstacles are so we can look at the appropriate steps we can take as a committee to open those avenues up.”

Reports of Jack Ma’s impending retirement are greatly exaggerated, it seems. Ma, the co-founder and executive chairman of Alibaba, has pushed back on claims that he is on the cusp of leaving the $420 billion Chinese e-commerce firm.

When reached for comment, Alibaba pointed TechCrunch to the SCMP report which claims Ma’s strategy will “provide [leadership] transition plans over a significant period of time.”

In order words, Ma isn’t abruptly leaving the company, but it seems that his role will be gradually reduced over time. Alibaba confirmed he’ll remain a part of the company while the succession plan is carried out. The exact details will be announced on Ma’s birthday, September 10.

That transition isn’t a new development. Ma stepped back from a daily role when he moved from CEO to chairman in 2013. Speaking at the time, he said that he would remain active and that it was “impossible” for him to retire but he did concede that younger people with fresher ideas should lead the business.

That’s exactly what has happened in the preceding years.

13-year Alibaba veteran Jonathan Lu stepped into Ma’s shoes as CEO. He led Alibaba when it went public in a record $25 billion IPO in 2015, but he was replaced in 2015 by Daniel Zhang after reportedly losing Ma’s confidence. Former COO Zhang leads the company today, although Ma’s presence still looms large and he is particularly involved in the political side of the business. That’s included a meeting with U.S. President Donald Trump, and various activities with national leaders in markets like Southeast Asia, where Alibaba has sought to leverage the colossal size of its business to make inroads in emerging markets and position its business for growth as internet access continues to increase.

“I sat down with our senior executives 10 years ago, and asked what Alibaba would do without me,” Ma told SCMP in an interview. “I’m very proud that Alibaba now has the structure, corporate culture, governance and system for grooming talent that allows me to step away without causing disruption.”

Another domino has fallen in Alex Jones’ media empire. Apple this week announced that it’s pulled the controversial conspiracy theorist/provocateur from the App Store this week, banning the Infowars app over violations to its “objectionable content” rules.

Slightly more specifically, the host was determined to have violated the TOS around “defamatory, discriminatory, or mean-spirited content, including references or commentary about religion, race, sexual orientation, gender, national/ethnic origin, or other targeted groups, particularly if the app is likely to humiliate, intimidate, or place a targeted individual or group in harm’s way.”

There’s been a cascade effect with many of the major platforms Jones has used to distribute his video content. Facebook, Google and Spotify have all pulled Infowars content from their respective platforms. This week, Twitter and Periscope banned him after widespread criticism.

Among other controversial comments, Jones has come under fire for suggesting that the Sandy Hook shooting, which resulted in the deaths of 20 elementary school students, was a hoax.

I’m deathly allergic to nuts, so I felt super excited when I heard about the Nima peanut sensor. I’ve ended up in the emergency room numerous times because there were nuts in something I thought did not contain nuts. With Nima, I could’ve tested those specific foods before consumption and probably avoided a trip to the ER.

Nima, a TechCrunch Battlefield alum, is gearing up to launch a peanut sensor, its second product, on September 12. The sensor is able to detect even the tiniest trace (10 parts per million) of peanut protein. To use Nima, you insert the food into a disposable test capsule, which goes into the device to figure out if there’s any peanut protein in the food. In under five minutes, the Nima sensor will tell you if your food is peanut-free.

The device connects to your phone via Bluetooth to enable the app to show your testing history, records of all the packaged foods yo’ve tried and a map of restaurants that Nima has tested for peanuts. To be clear, this sensor is just for peanuts. It does not test for all nuts, but Nima founder Shireen Yates told me the plan is to enable testing for additional nuts in the future.

The idea with Nima is not to suddenly ditch your Epi-Pen, an epinephrine shot designed to treat anaphylactic allergic reactions, but to provide one extra way to be confident about what you’re eating before you eat it. Based on two rounds of internal testing, Nima says there is a 97.6 percent accuracy rate.

Nima retails for $229 while the sensor plus 12 test capsules retails at $289. Nima launched its first product tested for gluten sensitivity. Check out the video at the top to learn more about Nima.

European Union lawmakers are facing a major vote on digital copyright reform proposals on Wednesday — a process that has set the Internet’s hair fully on fire.

Here’s a run down of the issues and what’s at stake…

Article 13

The most controversial component of the proposals concerns user-generated content platforms such as YouTube, and the idea they should be made liable for copyright infringements committed by their users — instead of the current regime of takedowns after the fact (which locks rights holders into having to constantly monitor and report violations — y’know, at the same time as Alphabet’s ad business continues to roll around in dollars and eyeballs).

Critics of the proposal argue that shifting the burden of rights liability onto platforms will flip them from champions to chillers of free speech, making them reconfigure their systems to accommodate the new level of business risk.

More specifically they suggest it will encourage platforms into algorithmically pre-filtering all user uploads — aka #censorshipmachines — and then blinkered AIs will end up blocking fair use content, cool satire, funny memes etc etc, and the free Internet as we know it will cease to exist.

Backers of the proposal see it differently, of course. These people tend to be creatives whose professional existence depends upon being paid for the sharable content they create, such as musicians, authors, filmmakers and so on.

Their counter argument is that, as it stands, their hard work is being ripped off because they are not being fairly recompensed for it.

Consumers may be the ones technically freeloading by uploading and consuming others’ works without paying to do so but creative industries point out it’s the tech giants that are gaining the most money from this exploitation of the current rights rules — because they’re the only ones making really fat profits off of other people’s acts of expression. (Alphabet, Google’s ad giant parent, made $31.16BN in revenue in Q1 this year alone, for example.)

YouTube has been a prime target for musicians’ ire — who contend that the royalties the company pays them for streaming their content are simply not fair recompense.

Article 11

The second controversy attached to the copyright reform concerns the use of snippets of news content.

European lawmakers want to extend digital copyright to also cover the ledes of news stories which aggregators such as Google News typically ingest and display — because, again, the likes of Alphabet is profiting off of bits of others’ professional work without paying them to do so. And, on the flip side, media firms have seen their profits hammered by the Internet serving up free content.

The reforms would seek to compensate publishers for their investment in journalism by letting them charge for use of these text snippets — instead of only being ‘paid’ in traffic (i.e. by becoming yet more eyeball fodder in Alphabet’s aggregators).

Critics don’t see it that way of course. They see it as an imposition on digital sharing — branding the proposal a “link tax” and arguing it will have a wider chilling effect of interfering with the sharing of hyperlinks.

They argue that because links can also contain words of the content being linked to. And much debate has raged over on how the law would (or could) define what is and isn’t a protected text snippet.

They also claim the auxiliary copyright idea hasn’t worked where it’s already been tried (in Germany and Spain). Google just closed its News aggregator in the latter market, for example. Though at the pan-EU level it would have to at least pause before taking a unilateral decision to shutter an entire product.

Germany’s influential media industry is a major force behind Article 11. But in Germany a local version of a snippet law that was passed in 2013 ended up being watered down — so news aggregators were not forced to pay for using snippets, as had originally been floated.

Without mandatory payment (as is the case in Spain) the law has essentially pitted publishers against each other. This is because Google said it would not pay and also changed how it indexes content for Google News in Germany to make it opt-in only.

That means any local publishers that don’t agree to zero-license their snippets to Google risk losing visibility to rivals that do. So major German publishers have continued to hand their snippets over to Google.

But they appear to believe a pan-EU law might manage to tip the balance of power. Hence Article 11.

Awful amounts of screaming

For critics of the reforms, who often sit on the nerdier side of the spectrum, their reaction can be summed up by a screamed refrain that IT’S THE END OF THE FREE WEB AS WE KNOW IT.

A coalition of original Internet architects, computer scientists, academics and others — including the likes of world wide web creator Sir Tim Berners-Lee, security veteran Bruce Schneier, Google chief evangelist Vint Cerf, Wikipedia founder Jimmy Wales and entrepreneur Mitch Kapor — also penned an open letter to the European Parliament’s president to oppose Article 13.

In it they wrote that while “well-intended” the push towards automatic pre-filtering of users uploads “takes an unprecedented step towards the transformation of the Internet from an open platform for sharing and innovation, into a tool for the automated surveillance and control of its users”.

There is more than a little irony there, though, given that (for example) Google’s ad business conducts automated surveillance of the users of its various platforms for ad targeting purposes — and through that process it’s hoping to control the buying behavior of the individuals it tracks.

At the same time as so much sound and fury has been directed at attacking the copyright reform plans, another very irate, very motivated group of people have been lustily bellowing that content creators need paying for all the free lunches that tech giants (and others) have been helping themselves to.

But the death of memes! The end of fair digital use! The demise of online satire! The smothering of Internet expression! Hideously crushed and disfigured under the jackboot of the EU’s evil Filternet!

And so on and on it has gone.

(For just one e.g., see the below video — which was actually made by an Australian satirical film and media company that usually spends its time spoofing its own government’s initiatives but evidently saw richly viral pickings here… )

For a counter example, to set against the less than nuanced yet highly sharable satire-as-hyperbole on show in that video, is the Society of Authors — which has written a 12-point breakdown defending the actual substance of the reform (at least as it sees it).

A topline point to make right off the bat is it’s hardly a fair fight to set words against a virally sharable satirical video fronted by a young lady sporting very pink lipstick. But, nonetheless, debunk the denouncers these authors valiantly attempt to.

To wit: They reject claims the reforms will kill hyperlinking or knife sharing in the back; or do for online encyclopedias like Wikimedia; or make snuff out of memes; or strangle free expression — pointing out that explicit exceptions that have been written in to qualify what it would (and would not) target and how it’s intended to operate in practice.

Wikipedia, for example, has been explicitly stated as being excluded from the proposals.

But they are still pushing water uphill — against the tsunami of DEATH OF THE MEMES memes pouring the other way.

Russian state propaganda mouthpiece RT has even joined in the fun, because of course Putin is no fan of EU…

The Society of Authors makes the very pertinent point that tech giants have spent millions lobbying against the reforms. They also argue this campaign has been characterised by “a loop of misinformation and scaremongering”.

So, basically, Google et al stand accused of spreading (even more) fake news with a self-interested flavor. Who’d have thunk it?!

Dollar bills standing on a table in Berlin, Germany. (Photo by Thomas Trutschel/Photothek via Getty Images)

The EU’s (voluntary) Transparency Register records Google directly spending between $6M and $6.4M on regional lobbying activities in 2016 alone. (Although that covers not just copyright related lobbying but a full laundry list of “fields of interest” its team of 14 smooth-talking staffers apply their Little Fingers to.)

But the company also seeks to exert influence on EU political opinion via membership of additional lobbying organizations.

And the register lists a full TWENTY-FOUR organizations that Google is therefore also speaking through (by contrast, Facebook is merely a member of eleven bodies) — from the American chamber of Commerce to the EU to dry-sounding thinktanks, such as the Center for European Policy Studies and the European Policy Center. It is also embedded in startup associations, like Allied for Startups. And various startup angles have been argued by critics of the copyright reforms — claiming Europe is going to saddle local entrepreneurs with extra bureaucracy.

Google’s dense web of presence across tech policy influencers and associations amplifies the company’s regional lobbying spend to as much as $36M, music industry bosses contend.

Though again that dollar value would be spread across multiple GOOG interests — so it’s hard to sum the specific copyright lobbying bill. (We asked Google — it didn’t answer). Multiple millions looks undeniable though.

Of course the music industry and publishers have been lobbying too.

But probably not at such a high dollar value. Though Europe’s creative industries have the local contacts and cultural connections to bend EU politicians’ ears. (As, well, they probably should.)

Seasoned European commissioners have professed themselves astonished at the level of lobbying — and that really is saying something.

Yes there are actually two sides to consider…

Returning to the Society of Authors, here’s the bottom third of their points — which focus on countering the copyright reform critics’ counterarguments:

The proposals aren’t censorship: that’s the very opposite of what most journalists, authors, photographers, film-makers and many other creators devote their lives to.

Not allowing creators to make a living from their work is the real threat to freedom of expression.

Not allowing creators to make a living from their work is the real threat to the free flow of information online.

Not allowing creators to make a living from their work is the real threat to everyone’s digital creativity.

Stopping the directive would be a victory for multinational internet giants at the expense of all those who make, enjoy and enjoy using creative works.

Certainly some food for thought there.

But as entrenched, opposing positions go, it’s hard to find two more perfect examples.

And with such violently opposed and motivated interest groups attached to the copyright reform issue there hasn’t really been much in the way of considered debate or nuanced consideration on show publicly.

But being exposed to endless DEATH OF THE INTERNET memes does tend to have that effect.

What’s that about Article 3 and AI?

There is also debate about Article 3 of the copyright reform plan — which concerns text and data-mining. (Or TDM as the Commission sexily conflates it.)

The original TDM proposal, which was rejected by MEPs, would have limited data mining to research organisations for the purposes of scientific research (though Member States would have been able to choose to allow other groups if they wished).

This portion of the reforms has attracted less attention (butm again, it’s difficult to be heard above screams about dead memes). Though there have been concerns raised from certain quarters that it could impact startup innovation — by throwing up barriers to training and developing AIs by putting rights blocks around (otherwise public) data-sets that could (otherwise) be ingested and used to foster algorithms.

Or that “without an effective data mining policy, startups and innovators in Europe will run dry”, as a recent piece of sponsored content inserted into Politico put it.

That paid for content was written by — you guessed it! — Allied for Startups.

Aka the organization that counts Google as a member…

The most fervent critics of the copyright reform proposals — i.e. those who would prefer to see a pro-Internet-freedoms overhaul of digital copyright rules — support a ‘right to read is the right to mine’ style approach on this front.

So basically a free for all — to turn almost any data into algorithmic insights. (Presumably these folks would agree with this kind of thing.)

Middle ground positions which are among the potential amendments now being considered by MEPs would support some free text and data mining — but, where legal restrictions exist, then there would be licenses allowing for extractions and reproductions.

And now the amendments, all 252 of them…

The whole charged copyright saga has delivered one bit of political drama already — when the European Parliament voted in July to block proposals agreed only by the legal affairs committee, thereby reopening the text for amendments and fresh votes.

So MEPs now have the chance to refine the parliament’s position via supporting select amendments — with that vote taking place next week.

There are 252 in all! Which just goes to show how gloriously messy the democratic process is.

It also suggests the copyright reform could get entirely stuck — if parliamentarians can’t agree on a compromise position which can then be put to the European Council and go on to secure final pan-EU agreement.

So, for example, she argues that amendments to add limited exceptions for platform liability would still constitute “upload filters” (and therefore “censorship machines”).

Her preference would be deleting the article entirely and making no change to the current law. (Albeit that’s not likely to be a majority position, given how many MEPs backed the original Juri text of the copyright reform proposals 278 voted in favor, losing out to 318 against.)

But she concedes that limiting the scope of liability to only music and video hosting platforms would be “a step in the right direction, saving a lot of other platforms (forums, public chats, source code repositories, etc.) from negative consequences”.

She also flags an interesting suggestion — via another tabled amendment — of “outsourcing” the inspection of published content to rightholders via an API”.

“With a fair process in place [it] is an interesting idea, and certainly much better than general liability. However, it would still be challenging for startups to implement,” she adds.

Reda has also tabled a series of additional amendments to try to roll back what she characterizes as “some bad decisions narrowly made by the Legal Affairs Committee” — including adding a copyright exception for user generated content (which would essentially get platforms off the hook insofar as rights infringements by web users are concerned); adding an exception for freedom of panorama (aka the taking and sharing of photos in public places, which is currently not allowed in all EU Member States); and another removing a proposed extra copyright added by the Juri committee to cover sports events — which she contends would “filter fan culture away“.

So is the free Internet about to end??

MEP Catherine Stihler, a member of the Progressive Alliance of Socialists and Democrats, who also voted in July to reopen debate over the reforms reckons nearly every parliamentary group is split — ergo the vote is hard to call.

“It is going to be an interesting vote,” she tells TechCrunch. “We will see if any possible compromise at the last minute can be reached but in the end parliament will decide which direction the future of not just copyright but how EU citizens will use the internet and their rights on-line.

“Make no mistake, this vote affects each one of us. I do hope that balance will be struck and EU citizens fundamental rights protected.”

So that sort of sounds like a ‘maybe the Internet as you know it will change’ then.

Other views are available, though, depending on the MEP you ask.

We reached out to Axel Voss, who led the copyright reform process for the Juri committee, and is a big proponent of Article 13, Article 11 (and the rest), to ask if he sees value in the debate having been reopened rather than fast-tracked into EU law — to have a chance for parliamentarians to achieve a more balanced compromise. At the time of writing Voss hadn’t responded.

Voting to reopen the debate in July, Stihler argued there are “real concerns” about the impact of Article 13 on freedom of expression, as well as flagging the degree of consumer concern parliamentarians had been seeing over the issue (doubtless helped by all those memes + petitions), adding: “We owe it to the experts, stakeholders and citizens to give this directive the full debate necessary to achieve broad support.”

MEP Marietje Schaake, a member of the Alliance of Liberals and Democrats for Europe, was willing to hazard a politician’s prediction that the proposals will be improved via the democratic process — albeit, what would constitute an improvement here of course depends on which side of the argument you stand.

But she’s routing for exceptions for user generated content and additional refinements to the three debated articles to narrow their scope.

Her spokesman told us: “I think we’ll end up with new exceptions on user generated content and freedom of panorama, as well as better wording for article 3 on text and data mining. We’ll end up probably with better versions of articles 11 and 13, the extent of the improvement will depend on the final vote.”

The vote will be held during an afternoon plenary session on September 12.

It’s go-time people. As in go apply right now to compete in TechCrunch Startup Battlefield Africa 2018 — do it now because in 48 short hours, the application window slams shut for good. Think you have the best early-stage startup in Sub-Saharan Africa? Do you dream on a global scale? Then come to Lagos, Nigeria on December 11 and launch your business to the world in front of the influential people who help make big dreams come true. Apply right here no later than September 10 at 5 p.m. PT.

Up to 15 of the best pre-Series A startups across Sub-Saharan Africa will compete head-to-head for the Startup Battlefield Africa 2018 championship, $25,000 in non-equity cash plus a trip for two to compete in Startup Battlefield in San Francisco at TechCrunch Disrupt 2019 (assuming the company still qualifies to compete at the time).

One of the great things about Startup Battlefield is that all participants — win or lose — benefit from broad exposure to investor love, media attention and access to an incredible network of influential technologists and entrepreneurs. That network, our Startup Battlefield alumni community, consists of more than 750 companies — including names like Dropbox, Mint, Vurb and many more — that have competed and gone on to collectively raise more than $8 billion in funds and generate 102 exits. The experience and advice these folks bring to bear can be invaluable.

Clearly our editors have a knack for picking winning startups, and they’ll scrutinize every eligible application. The chosen founders will all receive extensive, expert pitch coaching to prepare them for the six minutes they’ll have onstage to present a live demo to a panel of distinguished judges — and then answer all questions the judges throw at them. Five teams will move on to a second round of pitching and inquisition in front of a fresh set of judges.

Ultimately, one winner will rise above the rest to be Sub-Saharan Africa’s best startup. Will it be yours? The first step — before you apply — is to check whether you’re eligible to compete. Startups should:

Be early-stage companies in “launch” stage

Be headquartered in one of our eligible countries*

Have a fully working product/beta that’s reasonably close to, or in, production

Have received limited press or publicity to date

Have no known intellectual property conflicts

Apply by September 10 at 5 p.m. PT

Pretty standard stuff, right? So now that you’ve got that detail out of the way, don’t waste another moment. We want to see you strut your startup stuff in Lagos, Nigeria on December 11. Apply right here to compete in Startup Battlefield Africa 2018. The application window closes on September 10 at 5 p.m. PT.

*Residents in the following countries may apply:

Angola, Benin, Botswana, Burkina Faso, Burundi, Cameroon, Cabo Verde, Central Africa Republic, Chad, Comoros, Republic of the Congo, Democratic Republic of the Congo, Cote d’Ivoire, Equatorial Guinea, Eritrea, Ethiopia, Gabon, Gambia, Ghana, Guinea, Guinea-Bissau, Kenya, Lesotho, Liberia, Madagascar, Malawi, Mali, Mauritania, Mauritius, Mozambique, Namibia, Niger, Nigeria, Rwanda, Sao Tome and Principe, Senegal, Seychelles, Sierra Leone, Somalia, South Africa, South Sudan, Sudan, Swaziland, Tanzania, Togo, Uganda, Zambia and Zimbabwe. Notwithstanding anything to the contrary in the foregoing language, the “Applicable Countries” does not include any country to or on which the United States has embargoed goods or imposed targeted sanctions.