Eli Cahan is a medical student at NYU on leave to complete a master’s in health policy at Stanford as a Knight-Hennessey Scholar. His research addresses the effectiveness, economics, and ethics of (digital) health innovation.

More posts by this contributor

The coronavirus pandemic continues to spread with no signs of abating. Over 100,000 cases have been confirmed in almost 100 countries across the globe as of this writing. Some 4,000 deaths have been reported, 80% of which occurred in mainland China.

Preventive measures taken by the public sector and by global industry are already having widespread effects. In the past several days, Italy has officially imposed a whole-country lockdown and in the U.S., epicenter states such as California and New York have declared emergency status while instituting lockdowns on high-risk districts such as New Rochelle. Last week, the OECD cut global economic growth projections by half, and the JPMorgan Global Manufacturing Purchasing Manager’s Index (PMI) fell to its lowest level since 2009. Numerous companies including Apple and Nvidia have reported underwhelming earnings in recent quarters and have proceeded to cut their earnings guidance for the foreseeable future.

These economic impacts are in part related to disruption in demand for goods, due to quarantines and travel restrictions. However, more nefariously, economic pundits have expressed concern for supply-side disruptions: including staff productivity losses, supply-chain dysfunction, and facility closures.

According to a Dun & Bradstreet whitepaper released this week, 94% of Fortune 1000 companies have key elements of their supply chain housed directly within the epicenter of the outbreak in China. Supply-side shocks are much more difficult for central banks to contain by moves such as interest-rate cuts or financial stimulus. These typically serve to catalyze demand (through increased cash or borrowing power), but do not directly alleviate the kind of production paralysis capable of hamstringing global commerce.

How these preventive measures implicate startups

Startups are especially vulnerable to such supply-side disruptions, each of which is worth considering independently.

Decreases in staff productivity

Operating through lean organizational structures in which personnel often occupy cross-functional roles, decreases in staff productivity can create significant issues for interdependent activities at startups. The diversion of attention — due alternatively to the need to attend to personal needs (such as family caregiving, healthcare issues, or household concerns) or societal requirements (such as monitoring the development of the virus and state or federal reactions to it) — can make a cumulative impact over the days, weeks, and months of the outbreak.

The increased frequency of absences to attend to personal issues (such as individual healthcare or childcare amidst school closings) likewise presents a major challenge to fulfillment of contracts and other business obligations for startups. A CNBC survey conducted two weeks ago found that some 40% of companies had “stranded employees” facing some form of hurdle to commuting to the workplace. These figures are likely higher today.

Moreover, increased frequency of absences can be accompanied by heightened utilization of benefits (such as healthcare, sick leave, or family leave) in a short period, which startups may or may not have sufficient liquidity to support. These considerations around benefits are especially tenuous for startups in the gig economy, who may need to compensate affected employees regardless of their ability to perform tasks.

Supply-chain dysfunction

Turmoil in supply chains can bear significant consequences for startups across a diverse range of sectors, including technology and healthcare. This is especially the case given that these supply chains tend to be concentrated through only a selected group of vendors.

Since China is the world’s largest producer of industrial goods (in particular, basic parts), often at the world’s lowest prices, the widespread quarantines in the region are already proving debilitating: the number of bulk freight shipments has fallen over 70% since January and some 40% of China’s trucking capacity remains offline. And while American companies have sought to diversify away from China in recent years (partially due to political rhetoric), as the viral outbreaks spread to other major manufacturing countries (such as Vietnam, Bangladesh, and Mexico), supply chains for instrumental parts will likely face shortages, delays, and quality compromises.

In terms of services, startups often depend on regulatory, legal, and industrial collaborators for deliverables that are a prerequisite to their doing business. Disruptions in this “soft” supply chain capable of delaying essential credentialing, contracting, or data acquisition can prove incapacitating for startups. Furthermore, the proliferation of outsourcing (on the order of 14 million jobs in 2015) in service supply chains for critical tasks such as customer service and administrative workflows implies another dimension of vulnerability for service provision.

For either goods or services supply chains, to the extent that startups have relatively undiversified revenue streams — from a single or small group of contracts — these various forms of supply chain bottlenecks can be crippling (of basic fulfillment) in the short-run and compromising (of scaling and reputation) in the long-run.

Facility closures

Lastly, startups ought to consider the impact that closing and/or restricting their facilities can have on their performance.

Recent guidelines from the Centers for Disease Control (CDC) and Occupational Safety and Health Administration (OSHA) include recommendations for employers to develop “infectious disease outbreak response plans” that may require office/factory closures. Already, employers across the US are preparing for “social distancing measures” that are, overnight, converting physical workforces into virtual ones.

With the acceleration of community spread leading to diffusion of the virus out beyond US urban centers effected thus far (namely, New York City and San Francisco), more and more startups residing in neighboring suburbs may face closing their workplace.

Steps stakeholders in startups can take to provide stability

Taken together at face value, these supply-side considerations can seem overwhelming for startups already facing innumerable daily “fires” that need extinguishing. However, there are a variety of steps that CEOs, funders, and partners/clients of startups can take to inoculate themselves against the exogenous threat posed by coronavirus.

Startup CEOs ought to consider operational, organizational, and financial workarounds.

Operationally, they can take steps to prepare for a virtual workplace by establishing clear methods of digital communication and metrics to ensure productivity. They can also prepare for an “interrupted” workplace (in which employees require more time than usual for personal affairs and may be otherwise preoccupied) by embracing asynchronous workflows, laying out clear priorities for deliverables, and providing flexibility beyond standard office hours.

Organizationally, CEOs can cross-train employees and develop clear workflow protocols to insulate against staffing deficits that may arise. To fortify their organizational strategies, CEOs can identify weak points and/or major dependencies in their supply chains. In turn, they can seek to hedge against these where possible: either through delegation to additional firms or through integration internally.

Financially, to the extent possible, CEOs can shift their business models to prioritize revenue over growth in the short-run, ensuring liquidity against unexpected supply or demand shocks. This can be achieved through cost reduction or signing small-scale contracts (rather than “pursuing Moby Dick”). Alternatively, CEOs can consider raising anticipatory funding, even if in the ideal world they might defer a raise in pursuit of higher valuations.

Funders of startups are likewise well positioned to buffer against the fever state of startups. Providing leadership for early, anticipatory fundraising can support the stockpiling of dry powder to survive a prolonged siege by coronavirus (due, for example, to structural changes to the supply chain in the wake of the pandemic). It can also promote the creation of a war chest to allow startups to adapt under these abnormal circumstances.

Additionally, funders can leverage their expertise and networks to share learnings on dealing with similar challenges — therefore cultivating an ecosystem of resilience for potentially inexperienced leaders during the tumult associated with coronavirus.

Finally, partners and clients of startups have an important supporting role to play. It is very much in their own interest to ensure the vitality of startups upon which they depend: to avoid the costs of restructuring their own business models should a startup partner/vendor go defunct, and to empower their own innovation pipelines. As such, partner and client companies are well positioned renegotiate contractual terms to facilitate short-term flexibility while also ensuring long-term performance. Alternatively, they can redesign incentives and milestones in a way that can provide operational and financial security to startups for the time being without sacrificing the overall value expected in the more distant horizon.

Surviving coronavirus can bolster the immune systems of startups in the future

The coronavirus pandemic is likely to strain the capabilities of startups for the foreseeable future. Supply-side disruptions will present distinctive challenges to startups unlike those that typically crop up in a globalized economy.

Nonetheless, through keen vigilance, rapid adaptation, and comprehensive contingency planning, startups can survive the impending stress test. And in so doing, like white blood cells after a severe infection, surviving startups can develop resistance against the subsequent challenges they will inevitably face in their lifetimes.

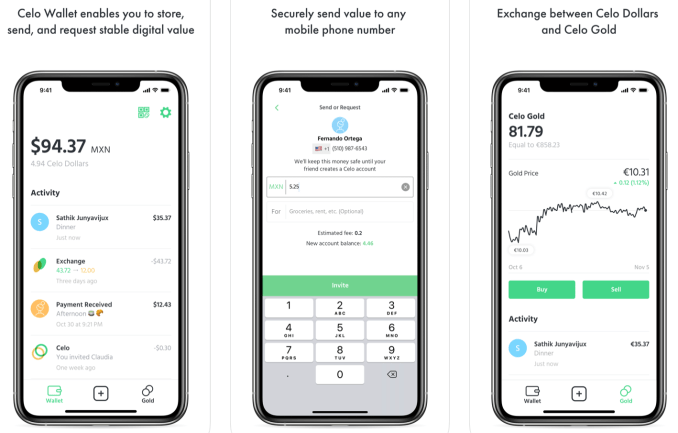

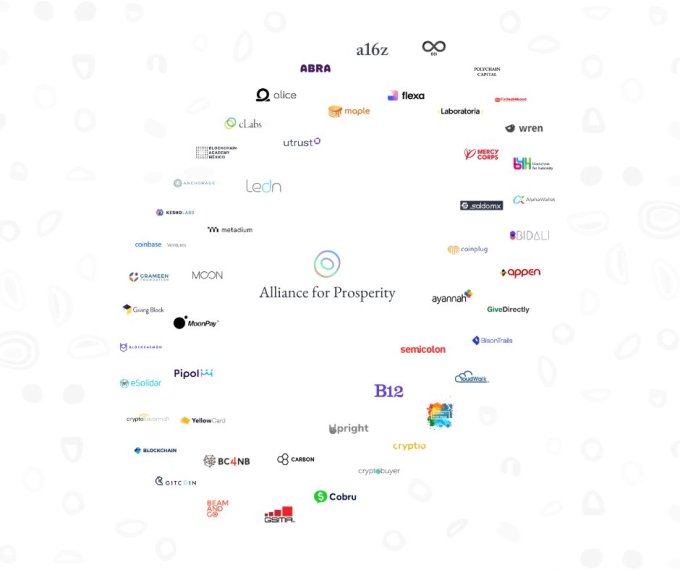

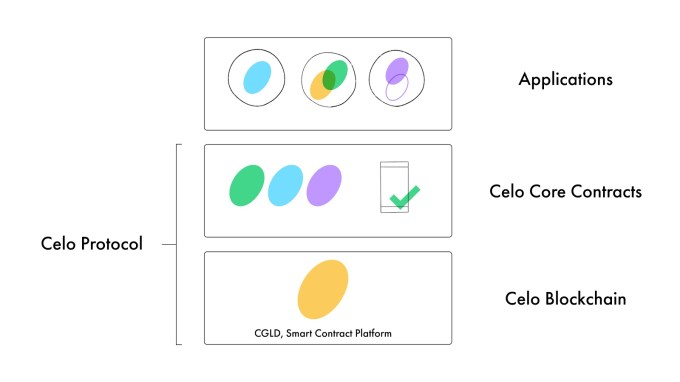

While it might not be a danger to the world financial system like Libra, it could be a danger to itself. At least on the anti-money laundering front, cLabs — the team that’s kicking off development of the Celo platform — has hired former Capital One head of enterprise risk management Jai Ramaswamy. Plus, the Celo founders come well pedigreed, including

While it might not be a danger to the world financial system like Libra, it could be a danger to itself. At least on the anti-money laundering front, cLabs — the team that’s kicking off development of the Celo platform — has hired former Capital One head of enterprise risk management Jai Ramaswamy. Plus, the Celo founders come well pedigreed, including