Amazon has said the number of demands for user data made by U.S. federal and local law enforcement have increased during the first half of 2020 than during the same period a year earlier.

The figures show that Amazon received 23% more subpoenas and search warrants, and a 29% increase in court orders compared to the first half of 2019. That includes data collected from its Amazon Echo devices and its Kindle and Fire tablets.

Breaking those figures down, Amazon said it received:

2,416 subpoenas, turning over all of partial user data in 70% of cases;

543 search warrants, turning over all of partial user data in 79% of cases;

146 court orders, turning over all of partial user data in 74% of cases.

The number of requests to the company’s cloud services, Amazon Web Services, also went up compared to a year earlier.

But it’s not clear what caused the rise in U.S. government demands for user data. A spokesperson for Amazon did respond to a request for comment.

But the company saw the number of overseas requests drop by about one-third compared to the same period a year earlier. Amazon rejected 92% of the 177 overseas requests it received, turning over partial user data in 10 cases and all requested data in four cases.

Amazon also said it received between 0 and 249 national security requests, flat from previous reports. Justice Department rules on disclosing classified requests only allow companies to respond in numerical ranges.

Amazon was one of the last major tech companies to issue a transparency report, despite mounting pressure from privacy advocates. But its report remains far lighter on details compared to its Silicon Valley rivals.

Formerly at Apple, Nils Mattisson is now CEO and co-founder of smart home tech company Minut.

If you look at the most successful startups today, you’ll find plenty of proof that the hardware-enabled service (Haas) model works: Peloton, Particle, Latch and Igloohome all rely on subscriptions along with product sales. Even tech giants like Apple are rapidly reinventing themselves as service companies.

Yet, if you currently rely on device sales, the prospect of changing your entire business model might seem daunting.

At Minut, we are building smart home monitors (privacy-safe noise, motion and temperature monitoring) and recently made the transition despite the lack of resources on the process. Here are the seven lessons we learned:

It is a question of when — not if.

The transition will have company-wide impact.

Your current and future target audience may differ.

Price should reflect the value for the customer. Your revenue should grow with theirs.

Avoid your free offer competing with your premium ones.

Be transparent (internally and externally) about the changes. Over-communicate.

Start the process early, check regularly with your team and set measurable targets.

Why subscriptions are the future of industry (and your startup)

Hardware has one advantage over software: customers understand there is a cost to your product. Now, this allows hardware startups to generate revenue with their first iteration, but it’s unsustainable as the company grows and needs to innovate: the software and user experience need continuous improvement and excellent support, just like in a software-only startup.

That’s why we see most hardware startups eventually launching a subscription model and limit what’s available for free. Even established companies — think Strava or Wink — often end up having to radically limit free features after years of operations.

Experienced founders and financial markets favor subscription models and recurring revenue. Market valuation multiples are typically much higher for companies that benefit from service revenue in addition to sales.

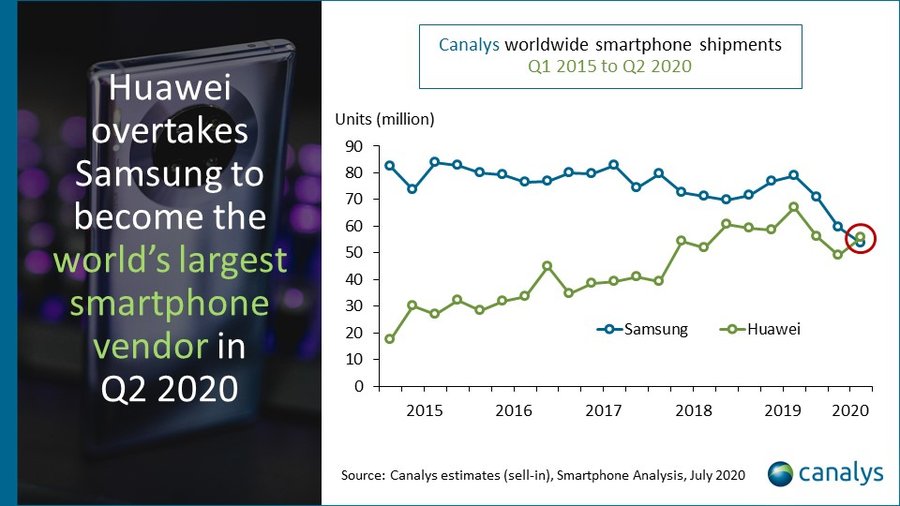

Things haven’t exactly been smooth sailing for Huawei in recent years. The company’s rapid trajectory has been disrupted by on-going battles with the U.S. government that have, among other things, blocked its access to Google apps and services. But a new report from Canalys paints a reasonably rosy picture as the hardware giant overtook Samsung to snag the top spot in global smartphone shipments for the second quarter of 2020.

The news is a milestone for a number of reasons, not the least of which is the fact that this is first time in nine years that neither Apple nor Samsung has been at the top of Canalys’ charts. Huawei’s figures were almost exclusively boosted by sales in its native China, which currently comprises more than 70% of its total figure.

Image Credits: Canalys

It’s important to note here, however, the fact that the company took the top spot by essentially shrinking at a less rapid rate than Samsung. Huawei’s overall figures are down 5% year-over-year. But that figure pales in comparison to Samsung’s 30% drop. The two Goliaths are currently at 55.8 million and 53.7 million, respectively.

Things were bad for the smartphone industry prior to COVID-19, but the pandemic certainly hasn’t helped overall, as people are less inclined toward shelling out hundreds to north of $1,000 for inessential upgrades. And, indeed, Huawei’s numbers dropped by 27% outside of China, but the overall slide was dampened by an 8% growth in China. Samsung, meanwhile, currently controls less than 1% of the Chinese market.

As for what this all means for the future, it seems that it may be difficult for Huawei to maintain its top spot. “Its major channel partners in key regions, such as Europe, are increasingly wary of ranging Huawei devices, taking on fewer models, and bringing in new brands to reduce risk” Canalys’ Mo Jia said of the report. “Strength in China alone will not be enough to sustain Huawei at the top once the global economy starts to recover.”

Stephen Ratner is a startup attorney who has advised emerging companies and venture funds. Prior to law school, he served as Deputy Press Secretary to Attorney General Eric Holder at the U.S. Department of Justice.

You’ve probably seen them on highway billboards and your Instagram feeds: startups promising to get it right on racial and gender inequity when it comes to employee pay. But how much progress has actually been made? Are companies even aware that upcoming stock option grants might worsen the very problem they claim to be fixing?

Last week, a top female executive at well-known equity management platform Carta resigned, alleging hypocrisy in the company’s public advertisements for equity compensation — or the now infamous statement by their CEO “Fair equity should be table stakes” — and their actual stance on correcting these wrongs within the company. This top executive was Emily Kramer, the very Harvard MBA brought on board in part to help improve stock option inequity at Carta and within its thousands of company users. These developments left me wondering what more can be done by leaders in equity management to help ameliorate these issues before they get harder to solve.

Anyone who’s worked closely to venture capital and tech in America knows that stock options are a key lever of attracting top talent, especially for companies with risky business models and low odds of success. Yet, equity compensation has received much less attention than cash pay. Further, this “paper wealth” can be invaluable to women and persons of color as the country attempts to attack its shameful income inequality. If you’ve had the opportunity to work with Carta, then you also know that gender and racial inequity in compensation exists with stock options too, not just cash.

Carta must act swiftly to implement a new feature across its entire platform: an alert to startup founders and legal administrators that upcoming option grants result in gender and racial inequity, when compared with the rest of the company’s employees doing similar work. Backed by the precept of “equal work, equal pay,” Carta has a unique opportunity to use its near informational monopoly to ameliorate “equity inequity” and make good on unkept promises. This feature ensures internal parity: that women and persons of color are compensated by equity grants on par with white and/or male colleagues performing the same work, in similar positions.

Having input equity compensation into Carta myself as a startup attorney, there’s no way I could have known if new grants were equitable across the capitalization table, unless Carta sent an alert or the company circulated its own report. The sad reality is that it’s way too challenging to independently perform this review on your own. Carta can because it’s a clearinghouse for equity compensation, used by more than 14,000 companies across the marketplace, with unique access to the tools and information required to know if a company’s astray from its stated values.

Wouldn’t it be helpful if Carta notified a client’s management team and lawyers that new grants didn’t achieve gender and racial equity while they still had a chance to adjust the numbers, before board grants? According to Carta’s own 2019 gender equity gap study published following a review of a sample of their own users’ capitalization tables, male founders represented 6.5% of equity holders but own 64% of all equity. Further, at the employee level, female employees own 49 cents in equity for every dollar men own. If companies affirmatively understood the gravity of their actions, the state of paper wealth in the United States would be far more equitable and inclusive.

I’d imagine social justice-minded companies would be happy to make adjustments to stock grants when it was easiest, not after the fact. After all, once options are granted by the board, it becomes an administrative hassle to redo. Yes, many companies do internal audits afterwards, uncovering inequities — but it’s usually too late or burdensome to make all of these employees whole, some of whom might have already departed. Let’s not forget that startups generally can’t even grant options to individuals no longer providing services to their company. A proactive, preemptive approach is not only reasonable, but required. Carta’s well-placed to make up for its broken promises by nudging users to get it right the first time.

Remember, later-stage companies have the money to perform comprehensive equity pay analysis, but early-stage companies often don’t. It’s at formation when inequities are easiest and cheapest to tackle, particularly for the promising early-stage, future unicorns that Carta spends so much time attracting in its successful Launch program — one that offers discounted services to retain startups as they grow. Attorneys, board members, startup operators — heck, even the most junior staff — need to be unafraid in using Carta as a tool to help bring these issues to light.

I want to believe that companies that promise racial and gender equity in compensation make it happen, but not all do. Some don’t care. But others are just overloaded with pitch decks, Slack notifications and the immense expectations of investors searching for big returns. It’s not an excuse, just a reality. What a difference it would make if Carta let management know of the problem before it was too widespread to fix.

PayPal has struck a deal with CVS Pharmacy to offer the ability to check out using PayPal’s payment services, including both PayPal and Venmo, at the register. The company announced this morning CVS will become the first nationwide retailer to allow customer to pay using either their PayPal or Venmo QR code at the register without fees. The payment will pull from funds available in the customer’s existing account balance, bank account, or from their debit or credit card, just as it would online. Venmo users will additionally have the option to pay with their Venmo Rewards.

CVS has committed to rolling out the technology across 8,200 U.S. stores in the fourth quarter of 2020.

PayPal introduced its new QR Code technology for buyers and sellers in 28 markets around the world in May.

The company described the offering as a way to make it safer for buyers and sellers to transact in person amid the coronavirus pandemic. Instead of having to hand over a payment card to be swiped or read, buyers could complete a transaction by aiming their smartphone camera at a QR Code that was either printed out or presented on the seller’s screen, for a touch-free way to pay.

The CVS deal builds on that existing technology, but scales it to a large, nationwide retailer.

Image Credits: PayPal

The new CVS checkout experience is being made possible through PayPal’s partnership with payments technology provider InComm, which PayPal describes as the “the first of a multi-year agreement” between the two payment technology companies. The agreement allows InComm to distribute PayPal QR Code technology through its cloud-based software updates, which will make the checkout feature available to retailers directly on their point-of-sale terminals.

The nature of PayPal’s relationship with InComm hints at this being a larger deal than just a single retailer. However, PayPal hasn’t officially announced which other retailers are in the pipeline.

This is hardly the first time PayPal has tried to bring its payment technology to the register.

Its first brick-and-mortar integration was back in 2012 with Home Depot. Soon after, PayPal expanded to 15 more national retailers, including names like JC Penney, Office Depot, Rooms To Go, Foot Locker, Barnes & Noble, and others, through relationships with half a dozen point-of-sale terminal makers, and partnered with POS software firm AJB. It later rolled out even more partnerships, including those with iPad POS solution provider Revel Systems and hardware maker NCR.

PayPal also launched a program to encourage retailers to switch to PayPal services, in its battle with Square. More recently, PayPal bought iZettle, the “Square of Europe,” to claim its place at point-of-sale.

Despite its advances, PayPal still lost the lead in the in-person mobile payments space to Apple Pay. In November 2019, Apple said its Apple Pay transactions topped 3 billion in its fiscal Q3, surpassing PayPal. Overall, however, Paypal is still ahead of Apple Pay in the digital payments space, but analysts have warned that Apple Pay is one of the “long-term competitive threats” to PayPal’s business.

PayPal, in other words, has to find a stronger foothold at the register. And it sees the pandemic as an ideal time to tout its touch-free payment technology.

“We know that in the current environment, buying and selling goods in a health-conscious, safe and secure way is front of mind for many people around the world. As the coronavirus pandemic has evolved, we have seen a surge in demand for digital payments to transition to include new and safe solutions for in-person environments and situations,” said John Kunze, PayPal Senior Vice President of Branded Experiences, in a statement. “Our rollout of QR codes for buyers and sellers incorporates the safety, security and convenience of using PayPal in person and enables ongoing social distancing requirements and safety preferences for in-person commerce,” he added.

Apple has another antitrust charge on its plate. Messaging app Telegram has joined Spotify in filing a formal complaint against the iOS App Store in Europe — adding its voice to a growing number of developers willing to publicly rail against what they decry as Apple’s app “tax”.

A spokesperson for Telegram confirmed the complaint to TechCrunch, pointing us to this public Telegram post where founder, Pavel Durov, sets out seven reasons why he thinks iPhone users should be concerned about the company’s behavior.

These range from the contention that Apple’s 30% fee on app developers leads to higher prices for iPhone users; to censorship concerns, given Apple controls what’s allowed (and not allowed) on its store; to criticism of delays to app updates that flow from Apple’s app review process; to the claim that the app store structure is inherently hostile to user privacy, given that Apple gets full visibility of which apps users are downloading and engaging with.

This week Durov also published a blog post in which he takes aim at a number of “myths” he says Apple uses to try to justify the 30% app fee — such as a claim that iOS faces plenty of competition for developers; or that developers can choose not to develop for iOS and instead only publish apps for Android.

“Try to imagine Telegram or TikTok as Android -only apps and you will quickly understand why avoiding Apple is impossible,” he writes. “You can’t just exclude iPhone users. As for the iPhone users, the costs for consumers to switch from an iPhone to an Android is so high that it qualifies as a monopolistic lock-in” — citing a study done by Yale University to bolster that claim.

“Now that anti-monopoly investigations against Apple have started in the EU and the US, I expect Apple to double down on spreading such myths,” Durov adds. “We shouldn’t sit idly and let Apple’s lobbyists and PR agents do their thing. At the end of the day, it is up to us – consumers and creators – to defend our rights and to stop monopolists from stealing our money. They may think they have tricked us into a deadlock, because we’ve already bought a critical mass of their devices and created a critical mass of apps for them. But we shouldn’t be giving them a free ride any longer.”

We also reached out to Apple for comment but the company also declined to provide an on the record statement regarding Telegram’s complaint. A spokesperson did point to a piece of analyst research, from earlier this year, which found iOS had a marketshare of 15% vs Android’s 85%. They also flagged a separate analyst report, which looks at commission rates charged by app and digital content stores and marketplaces — suggesting this shows that rates charged for similar types of stores are generally also around 30%.

So the company’s overarching argument against ‘app tax’ complaints continues to be the claim that: A) Apple can’t have monopoly power, given its relatively small mobile OS marketshare (vs Android); and B) the App Store fee is fair because it’s basically the same as everyone else charges. (On the latter point it’s true Google also takes a 30% cut via the Play Store. However the Android platform lets users sideload apps; whereas, on iOS, users would have to jailbreak their device to get the same level of freedom to freely install apps of their choice).

Apple’s arguments are also now being actively looked into by EU regulators. Last month the Competition Commission announced it’s investigating Apple’s iOS store (and Apple Pay) — saying a preliminary probe of the store had identified concerns related to conditions and restrictions applied by the tech giant.

Specifically vis-a-vis the App Store, the Commission said it’s looking at Apple’s mandatory requirement that developers use its proprietary in-app purchase system, and at restrictions it applies on the ability of developers to inform iPhone and iPad users of alternative cheaper purchasing possibilities outside of the App Store.

The investigation by EU regulators is just the latest in a series of major big tech antitrust probes under the bloc’s current competition chief, Margrethe Vestager — who has also been digging into Amazon and Facebook business practices in recent years, as well as hitting Google with a series of record-breakingantitrust fines.

Over in the US, meanwhile, lawmakers are also actively grappling with competition concerns that have long been attached to a number of tech giants — and are being exacerbated by the pandemic concentrating platform power. Apple is one of the tech giants of concern, though not, seemingly, top of US lawmakers’ target list.

Yesterday, a hearing of the House Antitrust Subcommittee took testimony from four big tech CEOs: Amazon’s Jeff Bezos, Apple’s Tim Cook, Facebook’s Mark Zuckerberg and Google’s Sundar Pichai — with Pichai, Bezos and Zuckerberg getting the most questions from lawmakers.

Cook did face a number of questions around how the company operates the App Store, though — including about the commission it charges developers and a specific line of enquiry on why it had removed rival screen time apps. Asked whether Apple could ever raise its 30% take on app subscriptions Cook sought to sidestep the question, saying the fee had remained unchanged since the launch of the store.

He then followed up by arguing Apple faces huge competition for developers — citing alternatives platforms such as Windows and Xbox as also fiercely vying for developers, and likening the competition to attract developers as akin to “a street fight for market share”.

The contention from complainants like Spotify and Telegram is that Cook’s claim of Apple facing fierce competition for developers’ wares, from its position as the world’s second largest smartphone OS by marketshare, does not stand up to scrutiny. But it’ll be up to EU regulators to determine how to define the market for smartphone apps and, flowing from that, whether they identify harm or not.

This week, TechCrunch covered a startup called Hevo raising $8 million, and Paragon, which raised a $2.5 million seed round. Hevo is a “data pipeline startup” that helps “clients’ employees to integrate data from more than 150 different sources — including enterprise software from Salesforce and Oracle without requiring a technical background, we reported.

Paragon, part of Y Combinator’s Winter 2020 batch, is a developer productivity-focused service that “makes it easier for non-technical people to be able to build out integrations using our visual workflow editor” according to its co-founder Brandon Foo. Paragon wants to “bring the benefits of low code to product and engineering teams and make it easier to build products without writing manual code for every single integration” to help “streamline the product development process,” Foo added.

The trend that we noted last week that no-code and low-code startups are raising lots of capital is still hot.

But startups aren’t the only companies working in this space: Apple has long had a foot in the domain via its subsidiary Claris, which rebranded to that name last year after running under the FileMaker moniker. At the time, Claris CEO Brad Freitag told TechCrunch that his company’s vision was to make “powerful technology accessible to everyone.”

That wasn’t merely cliché: Claris’ best-known product, FileMaker, helps users build low-code apps, and its second product is called Connect, a service that helps users link APIs using low-code tooling.

Given that Claris has been in the no-code, low-code space for longer than most, TechCrunch caught up with Freitag again to chat about recent growth in the market category, what he thinks of the low-code terminology, and, of course, his take on startups in the niche.

Trade tensions between China and the U.S. have not stopped Chinese companies from eyeing to list on American stock exchanges. Li Auto, a five-year-old Chinese electric vehicle startup, raised $1.1 billion through its debut on Nasdaq on Thursday.

The Beijing-based company is targeting a growing Chinese middle class who aspire to drive cleaner, smarter, and larger vehicles. Its first model, sold at a subsidized price of 328,000 yuan or $46,800, is a six-seat electric SUV that began shipping end of last year.

Li Auto priced its IPO north of its targeted range at $11.5 per share, giving it a fully diluted market value of $10 billion. It also raised an additional $380 million in a concurrent private placement of shares to existing investors.

The IPO arrived amid a surge of investor interest in EV makers. Tesla’s shares have skyrocketed in the last few quarters. Li Auto’s domestic rival Nio, which raised a similar amount in a $1 billion float in New York back in 2018, also saw its stock price rally in recent months.

Li Auto is one step ahead of its Chinese peer Xpeng in planning its first-time sale. The six-year-old competitor said last year it may consider an IPO. Last month, a source told South China Morning Post that Xpeng was getting ready for the listing.

Founders of China’s emergent EV startups are often shrewd internet veterans who are well-connected in the venture capital and marketing world, attracting investment dollars in the billions. Li Auto, for instance, counts China’s food delivery mogul Wang Xing, boss of Meituan Dianping, as its second-largest shareholder after its CEO Li Xiang. TikTok parent ByteDance shelled out $30 million in its Series C round.

Investors are in part emboldened by Beijing’s national push to electrify China’s auto industry. The question, then, is whether these startups have the right talent and resources to pull things off in an industry that traditionally demands a much longer development cycle.

Wallace Guo, a managing partner at Li Auto’s Series B investor Taihecap, admitted that “the nature of auto consumption, unlike internet products evolving through trial and error, manufacturing a car, is a strategic move with sophisticated system, very long value chain, requiring huge investment and resources and any error can be fatal.”

Mingming Huang, chief executive of Future Capital, said that “it was a no brainer in 2015 to be the first investor” in Li Auto. The venture capitalist said Li, who ran a popular car-buying online portal before getting into manufacturing, “has the rare combination of being a relentless talent as well as a top-notch product manager that excels in creating value for all stakeholders.”

Customers testing Li Auto’s SUV in China. Photo: Li Auto

Both investors believed Li Auto has picked the right path of zeroing in on extended-range electric vehicles. EREVs come with an auxiliary power unit, often a small combustion engine, that ensures cars can still operate even when a charging station is not immediately available, a shortage yet to be solved in China.

As my colleague Alex pointed out, Li Auto is on a trajectory similar to that of its peer Nio, going public after a short history of delivering to customers. The startup only began shipping its first model last December and delivered just over 10,000 units as of June, its prospectus showed.

The startup is still deep in the red, losing 2.44 billion yuan ($350 million) in 2019, up from a net loss of 1.53 billion yuan in 2018. It did finish the first quarter of 2020 with a gross profit of $9.6 million after it began monetization.

Its annual revenue — which comprised mostly of car sales and a small portion from services like charging stalls — stood at 284 million yuan ($40.4 million) in 2019, a tiny fraction of Nio’s $1.12 billion. But Nio also amassed a greater net loss of $1.62 billion in the same year. In contrast, Tesla has been profitable for four straight quarters.

Li Auto’s investors are clearly bullish that the Chinese startup can one day match Tesla’s commercial success.

“Xiang has a deep understanding of the preferences and pain points of car owners and drivers in China. Li Auto is the first in China, to successfully commercialize extended-range electric vehicles, solving the challenges of inadequate charging infrastructure and battery technologies constraints,” Huang asserted.

“The company is able to get positive gross margin when selling the first batch of vehicles and thus with its growth in sales volume, its gross margin was well above competitors and can live long enough to become a ten billion-dollar company with this healthy business model,” said Guo.

While we often focus on the mega rounds that drive big startup valuations, the reality is that every startup has to start somewhere and find that first check that few to no investors are willing to actually write.

Notation though has made that first hurdle its key differentiator.

Across its first two funds, an $8 million vehicle raised in 2015 and a $28 million second fund with more institutional capital in 2017, the New York City-based firm has been intensely focused on the earliest stage startups: founders thinking about spinning out of companies, engineers with ideas scrawled on whiteboards, product developers with PowerPoints or maybe a workable MVP.

For the firm’s two GPs, Nick Chirls and Alex Lines, that stage of a startup’s life was both the most rewarding stage to invest in and where they had the most experience. Formerly, the two had worked at Betaworks, the fund / workspace / incubator / community that has helped bring companies like Giphy to life.

Now, with the pandemic in full swing, the duo are tripling down on their thesis.

The firm announced today the launch of its third fund, a $42 million vehicle that was “closed it in the depths of the coronavirus” according to Chirls. In addition, he highlighted the firm’s first external hire of Katherine Wu as a principal, who officially joined roughly a year ago.

In addition to investing, she will be launching with Lines and Chirls a new program called Notation Moonlight this September, which is designed as a community of up-and-coming tech leaders who are considering building a company someday.

Chirls said that while Silicon Valley has a lot of infrastructure in place to help founders go down the path of starting a company, such resources were less prevalent in New York City and other smaller startup ecosystems. With Moonlight, “we want to begin to build that same set of resources and community for folks that are going to start a company but haven’t yet,” he said.

Wu noted that more direct outreach through initiatives like Moonlight could help improve the pipeline of founders, particularly from less traditional backgrounds or from under-represented groups. “If we’re being totally honest in New York City, entrepreneurship and startups, they’re not as deeply entrenched into everyone’s minds as [they are] in San Francisco and Silicon Valley,” she said. The goal is to “just give them the tools … essentially bring our network to them.”

The initial cohort is targeted at somewhere between 15 and 20 potential founders. Moonlight will not take equity, doesn’t require its participants to give up their day jobs, and essentially will act as a decentralized community for participants to talk to one another and think through the steps of fleshing out products, investigate interesting markets and build friendships that can help make the startup experience a little less lonely.

As for Notation’s new fund, there are some small tweaks. The bulk of the fund will remain devoted to the same geo — New York City — and the same general markets, which include enterprise software and infrastructure, blockchain, and other technical projects. Wu will add a bit more of a consumer flair to the team’s investment interests, and Notation is also intending to invest a small chunk of its fund in smaller startup ecosystems like Boston and Atlanta, where the firm recently made its first investment.

They are looking at these markets “For all the same reasons we loved New York five years ago — there’s great talent, there’s not enough capital, there’s not enough first check firms,” Chirls explained. That’s a sentiment that every founder can empathize with, and Notation now has even more capital to solve it.

There are more than 300,000 congregations in the U.S., and entrepreneurs are creating billion-dollar companies by building software to service them. Welcome to church tech.

The sector was growing prior to COVID-19, but the pandemic forced many congregations to go entirely online, which rapidly accelerated growth in this space. While many of these companies were bootstrapped, VC dollars are also increasingly flowing in. Unfortunately, it’s hard to come across a lot of resources covering this expanding, unique sector.

Market map

In broad terms, we can split church tech into six categories:

church management software (ChMS)

digital giving

member outreach/messaging

streaming/content

Bible study

website and app building

Horizontal integration is huge in this sector, and nearly all the companies operating in this space fall into several of these categories. Many have expanded through M&A.

Church management software: Almost all are SaaS businesses, mostly using cloud hosting. Typical features include workflow management, virtual check-in for events, a database of members and online scheduling. Examples include Elvanto and One Church.